2025 Mid-Year Financial Outlook

Navigating Trump's Tariffs, Fed Liquidity, & Portfolio Risks

As we cross the halfway point of 2025, it's critical to reflect on our analysis and forecasts from earlier this year—and assess what's ahead for markets and your portfolio.

Tariffs, Trade, & Historical Parallels

When President Trump reclaimed the presidency, optimism surged regarding potential economic policies focused on lower deficits & reduced government spending. However, despite campaign promises, Trump’s administration implemented aggressive tariff policies, significantly impacting global trade.

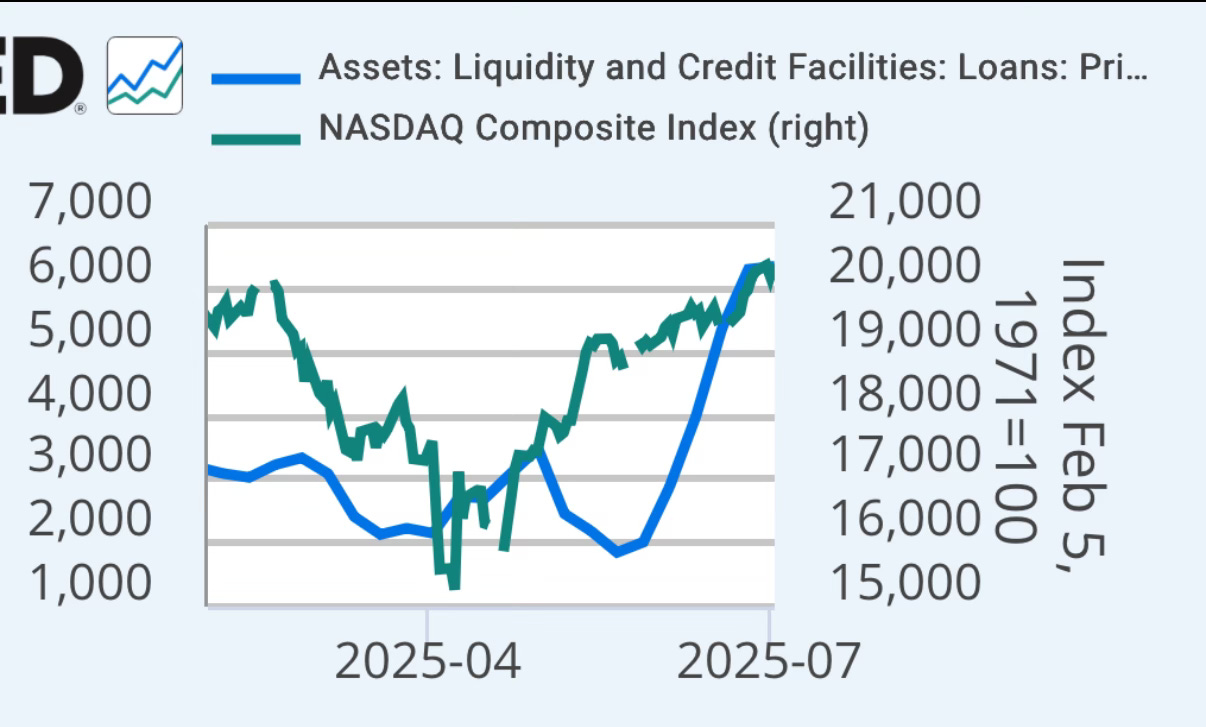

Initially, we warned that proposed tariffs could lead to severe market declines (HERE). Indeed, markets rapidly fell -25% in response. Only Trump's swift reversal and the Fed’s unprecedented liquidity injections—including the discount window, repurchase agreements, and overnight repos—halted the decline, pushing markets to all-time highs, today.

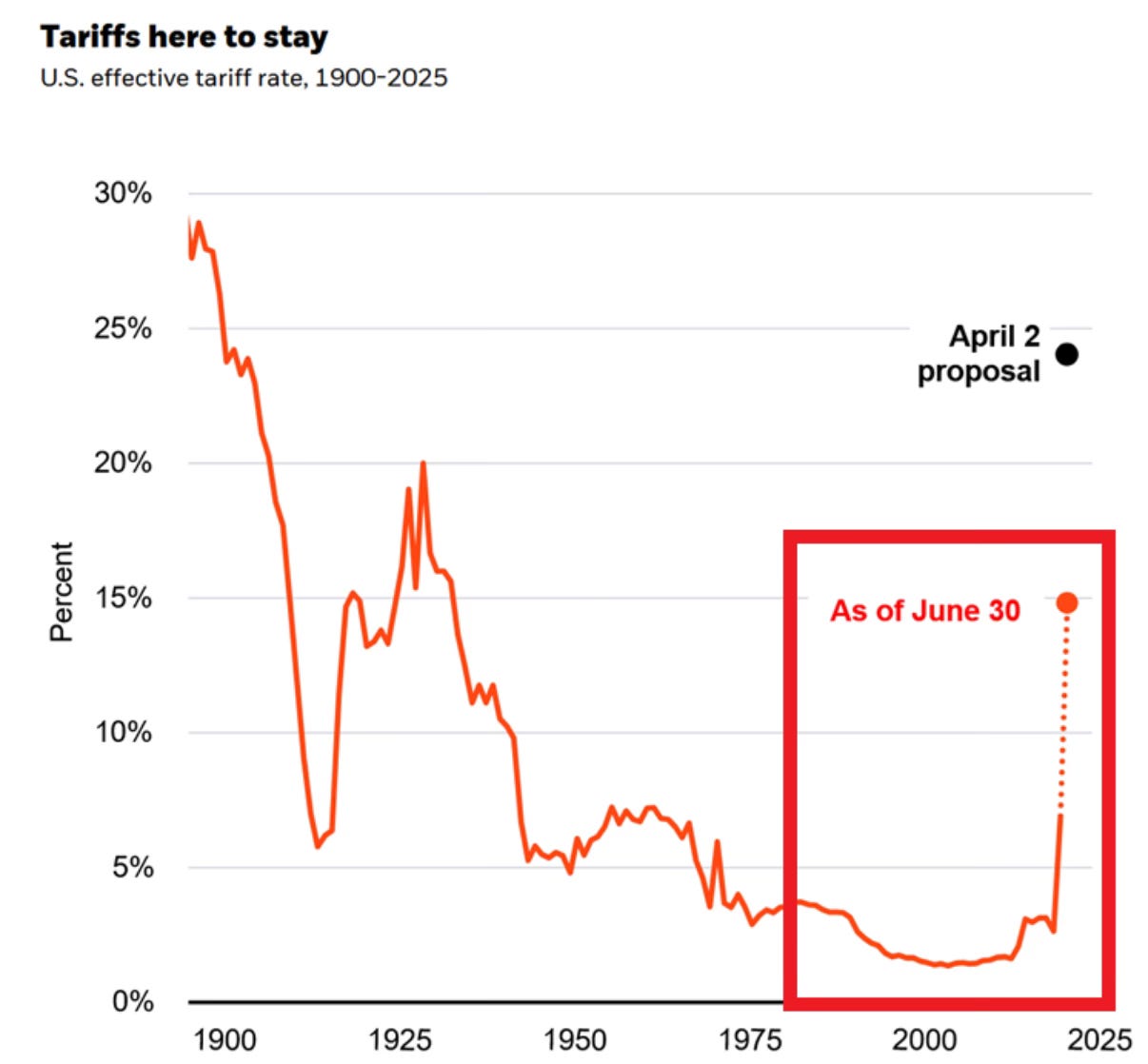

However, the Trade War isn’t resolved—it’s postponed. Trump's self-imposed deadline for tariff negotiations is approaching. Current tariffs with key partners like China, Europe, Canada, and Mexico already exceed levels seen since Herbert Hoover’s presidency.

Without substantial deals, Trump’s original tariff rates from April could re-emerge, surpassing Hoover’s tariffs of 1930, igniting economic uncertainty reminiscent of the Great Depression. Hoover's tariffs triggered global trade wars, severely contracting international trade and dramatically exacerbating the global economic downturn. A repeat of such aggressive tariff policies today risks plunging international markets into turmoil, disrupting supply chains, and significantly increasing costs for both consumers and businesses, resulting in substantial job losses and a potential recession.

Current Economic Indicators Already Reflect Damage

Unemployment Rising: Continuing jobless claims are persistently hovering near 2 million (up about 9% since Jan 2025), reflecting broader labor market weaknesses. More concerning is the consistent increase in the four-week moving average for initial unemployment claims. This signals that job losses are becoming more systemic, rather than isolated incidents. Should tariffs escalate further, these unemployment figures could surge as businesses—particularly in manufacturing and export-reliant sectors—are forced to cut jobs due to declining orders and increasing costs. This sharp decline underscores the immediate and detrimental impact tariffs have on American businesses’ ability to compete abroad. With foreign markets retaliating against U.S. tariffs by reducing their purchases of American products, businesses face diminished revenues, shrinking profit margins, and potential layoffs. If the trend continues, it will severely restrict economic growth, reduce wages, and negatively impact the broader U.S. economy.

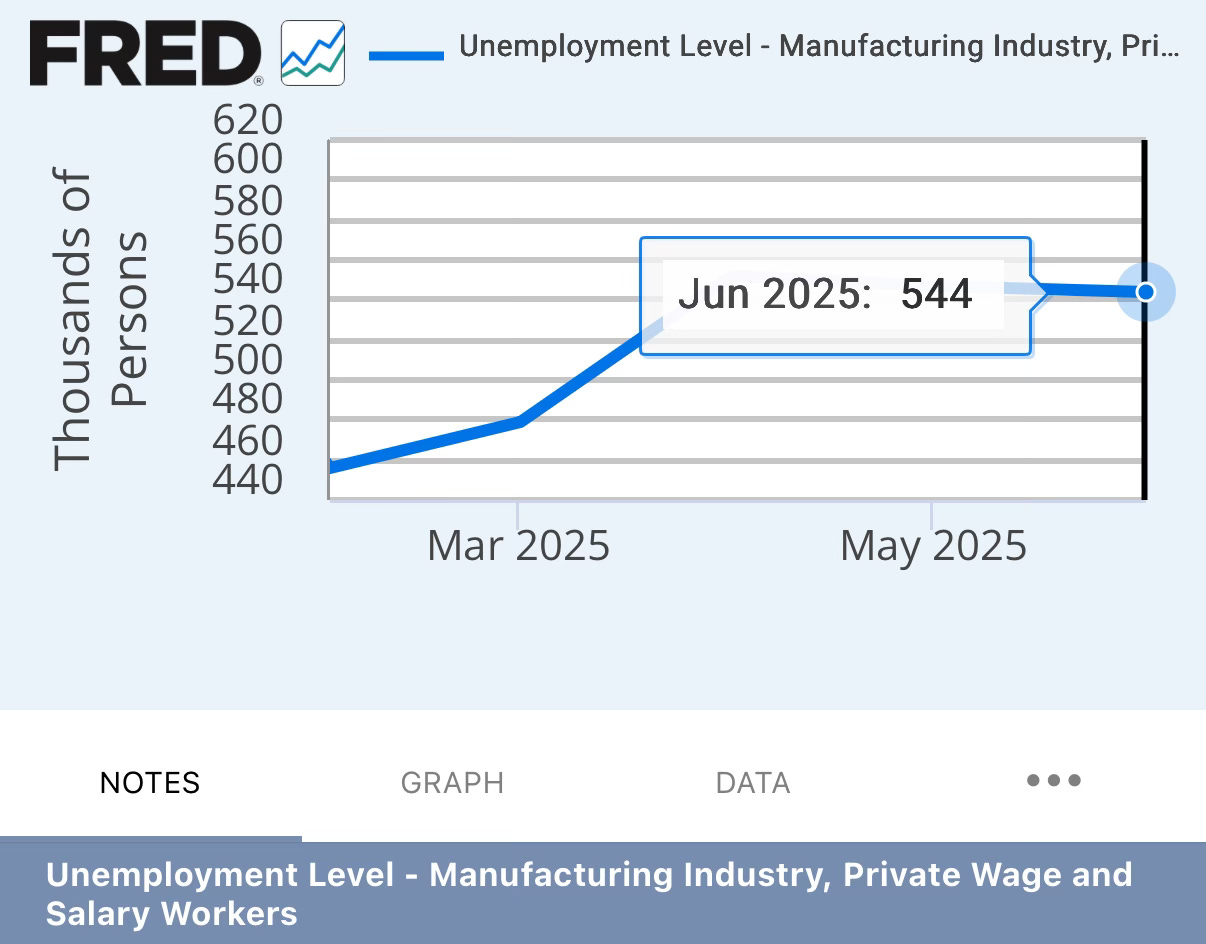

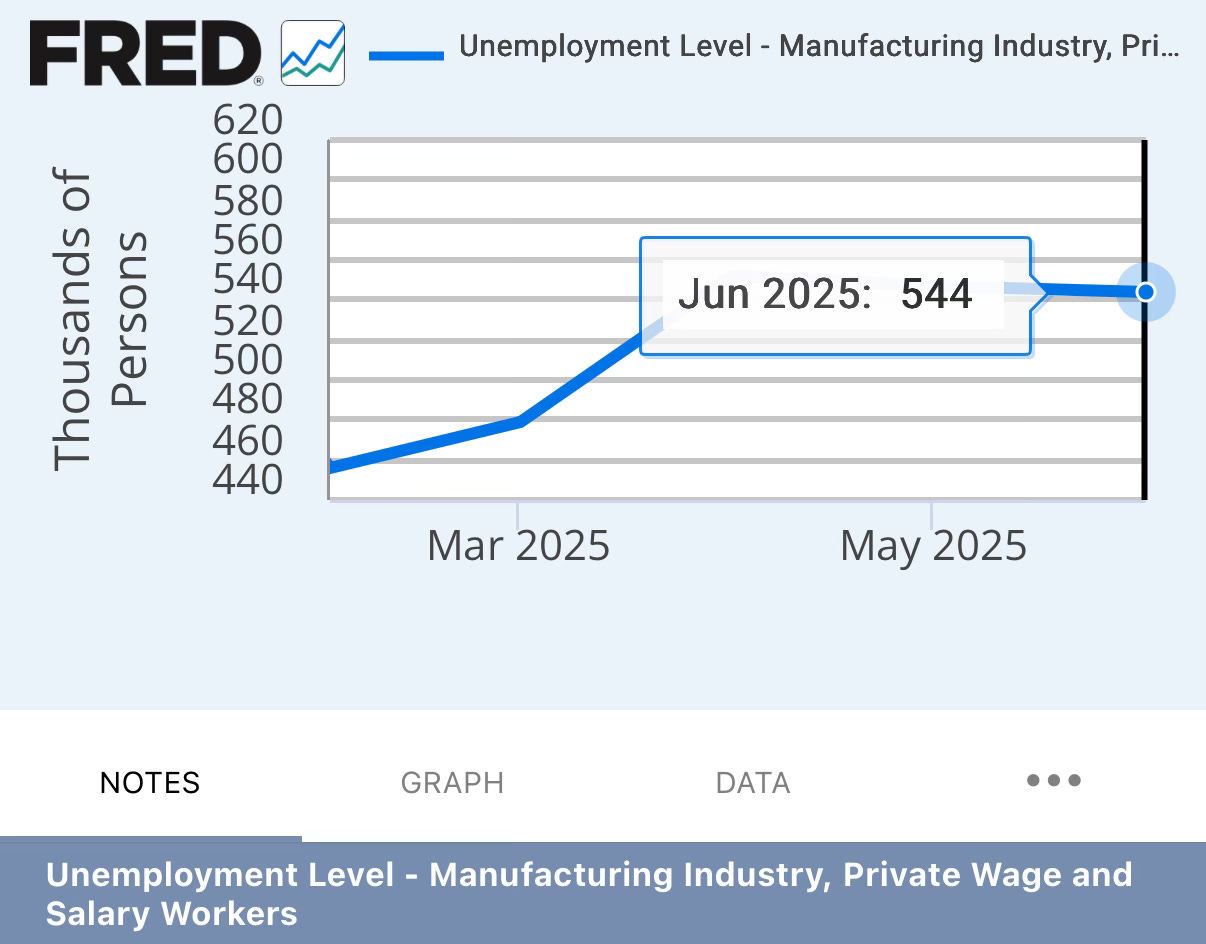

Manufacturing jobs declining: Direct result of reduced foreign demand for American-made goods, unemployment for Americans in manufacturing is up 19% since February. This is one of the largest sector increases of unemployment in what’s suppose to be a new boom.

Trade Deficit Widening: In June alone, the U.S. trade deficit ballooned to $71 billion from $60 billion the previous month, primarily driven by a -4% month-over-month decline in exports.

Protect Your Portfolio Now

We anticipated and accurately called key developments at the start of the year:

Advocated owning gold since $2,800/ounce; gold has surged, outperforming equities.

Warned of Fed-driven market rallies detached from fundamental earnings growth.

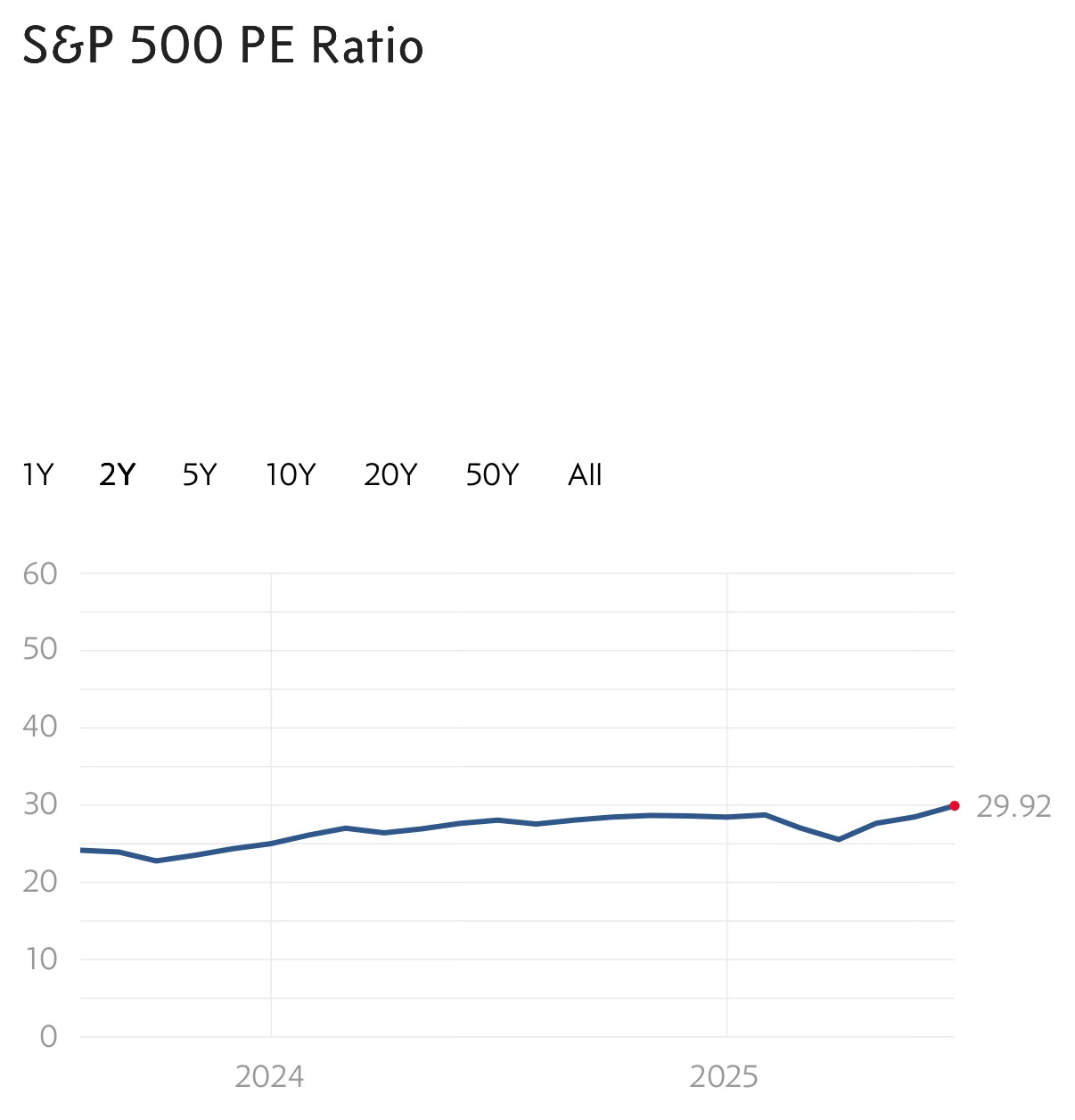

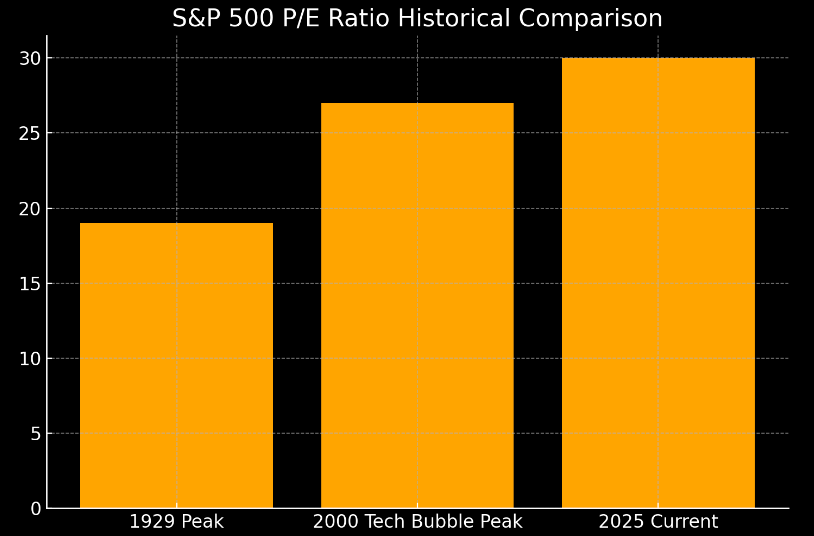

The recent Fed-induced market pump has inflated stock valuations dangerously. The S&P 500 currently trades at an eye-watering 30 times earnings.

**Higher than both the 1929 peak (19x) and 2000 tech bubble peak (27x).

Historically, at these valuation levels, subsequent returns average significantly lower or negative, reflecting severe mean reversion risks.

Keep reading with a 7-day free trial

Subscribe to The Coastal Journal to keep reading this post and get 7 days of free access to the full post archives.