AI’s Dark Compute Moment: Efficiency Collides With $600+ Billion in CAPEX

Why AI’s Cost Curve Is Collapsing Faster Than CAPEX Can Earn It Back — And What That Means for Infrastructure Returns and Stock Multiples

In Good Will Hunting, the loudest guy in the bar makes a basic economic mistake: he assumes the price tag proves the value. A $150,000 education must confer superiority because it costs $150,000. Will Hunting doesn’t dismiss education—he attacks the logic. The knowledge isn’t exclusive; it’s sitting there for anyone willing to do the work. And then he lands the line that matters: you dropped $150 grand on an education you could’ve gotten for $1.50 in late fees at the public library.

That same price-tag illusion is being industrialized into the AI capex boom. **The hyperscalers—Microsoft, Google, Amazon, Meta—**are committing staggering sums to GPUs, and data-center capacity on the belief that scarce compute today becomes pricing power tomorrow. That’s the sales pitch. The risk is straightforward: capital commitments are fixed, but the environment isn’t. When conditions change, those commitments become constraints.

So what does that mean for the 2026 AI buildout narrative?

Frontier-scale deployments—premium GPUs, premium networking, premium power—are being marketed as the onlycredible route to dominance. The implied logic is seductive: scale first, profits later.

But enterprise buyers don’t buy mythology; they buy outcomes. As soon as budgets tighten and scrutiny rises, procurement starts asking the question that matters: how much “frontier” do we actually need? And the moment that question becomes standard, the premium tier has to justify itself every quarter, not just in investor decks.

If you’re a CFO locking into multi-year data-center commitments in 2026, there’s one rule you don’t get to ignore: you can’t underwrite venture-style returns with infrastructure-style rigidity. When the economics move faster than the asset can be depreciated, the spreadsheet doesn’t bend—it breaks.

Dark Fiber History

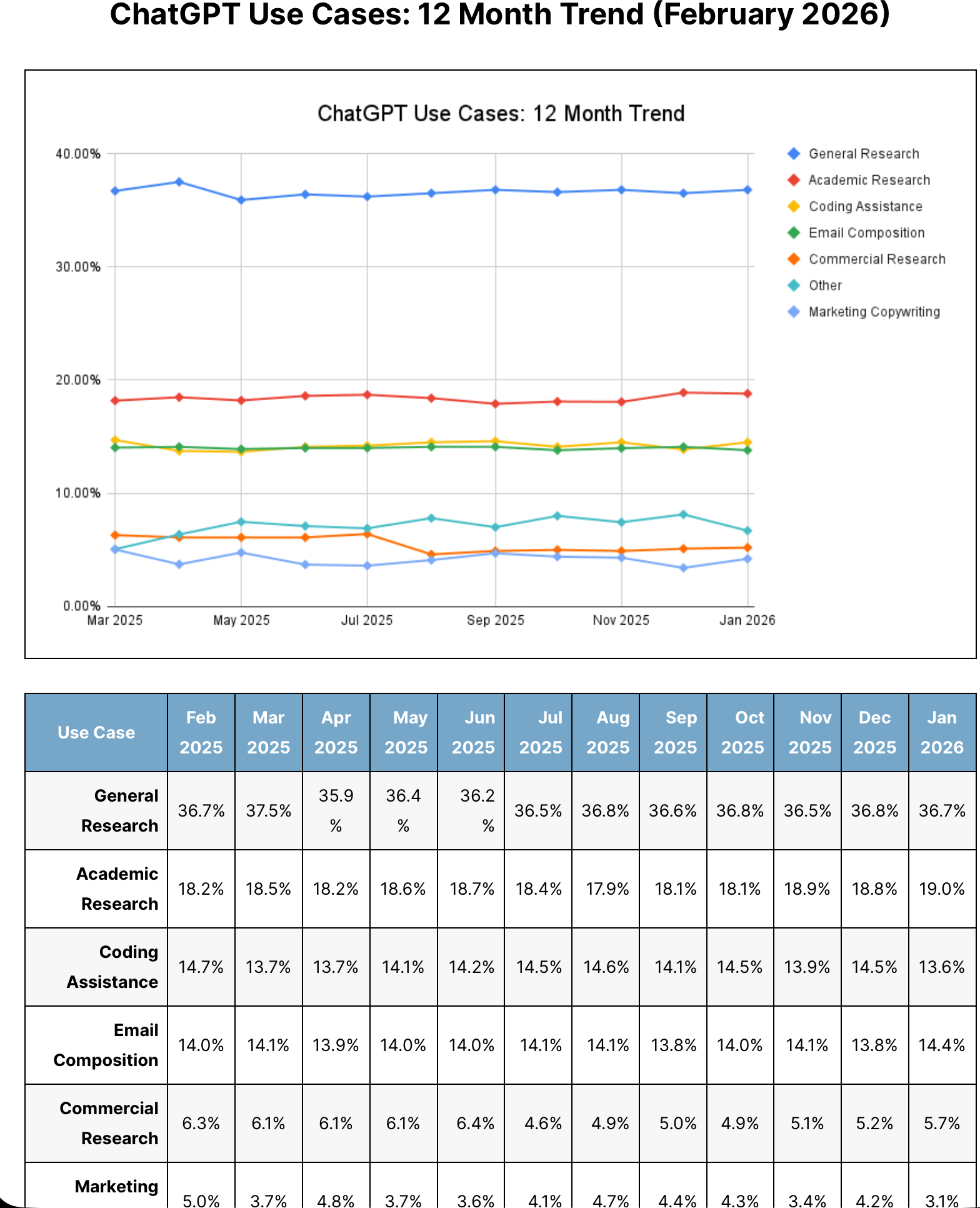

We’ve witnessed this dynamic before. Dark fiber didn’t fail because the internet was fake; it failed because the infrastructure grew faster than the demand that could be monetized. Even today, a small anomaly emerges in ChatGPT data: “General Research” usage has remained consistently in the mid-30% range (~36–37%) over the past year, never surpassing 40%.

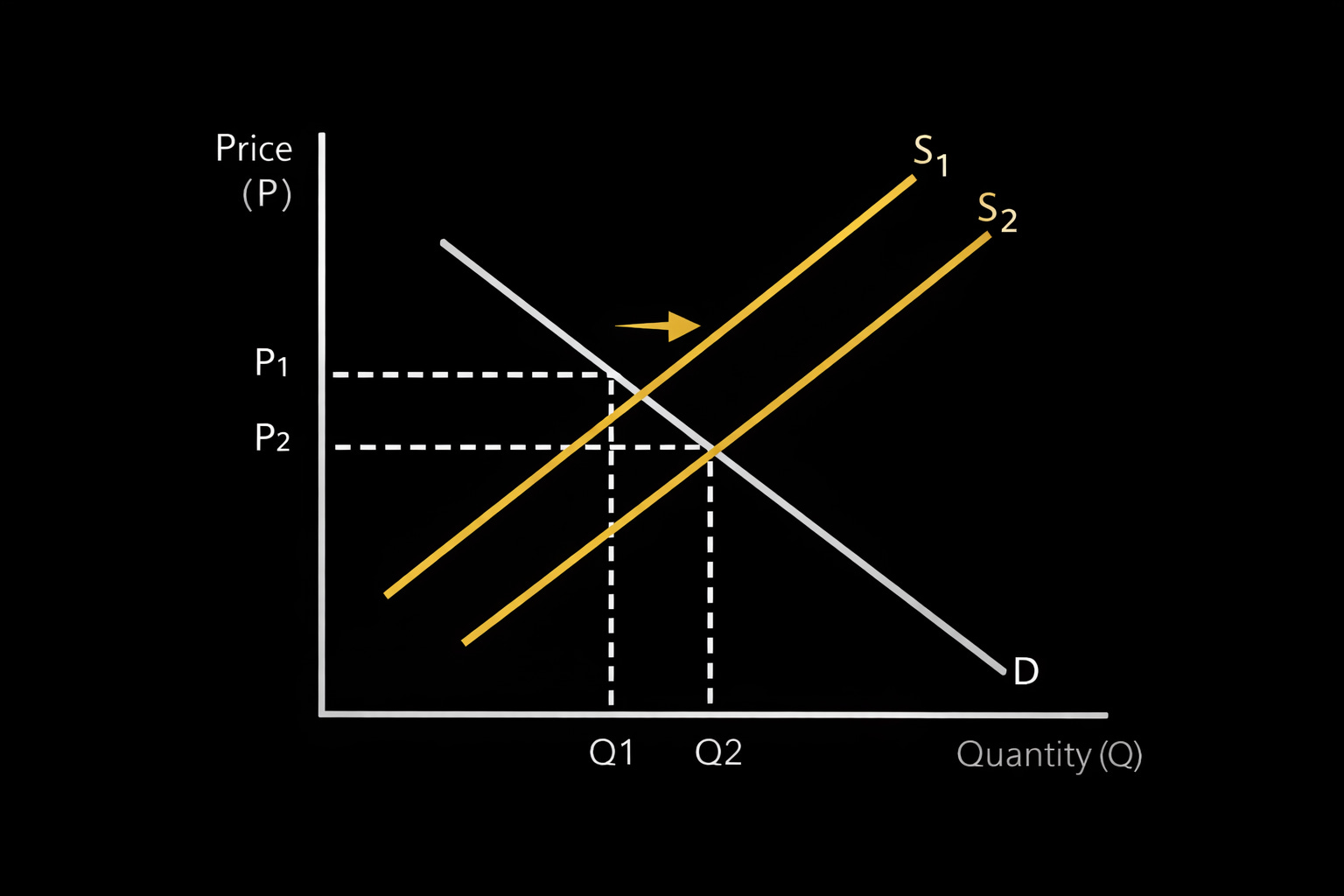

You can have 800 million users and still not have enough paid consumption growth to match capacity growth. When compute supply (GPU-hours) compounds faster than billable demand, utilization mathematically declines (Demand ÷ Supply), pricing clears the surplus, and returns compress.

At the peak, fiber capacity (supply) was growing at roughly 100% per year while internet traffic usage (demand) grew closer to 50%. When supply compounds materially faster than demand—even in a revolutionary technology—pricing breaks. (shown below)

The AI analogue is emerging now: hyperscalers are targeting roughly ~$610B of capex in 2026, while revenue-grade demand grows far more slowly. If AI data centers expand faster than monetization, stress shows up in utilization, then pricing, then returns.

When the investment thesis is “capex equals stock price upside,” the market often misses the second-order effect: the more capacity you fund, the faster the product commoditizes. Prices reset lower, returns get pushed out, and the winners are determined by timing, leverage, and supply discipline—not optimism. Infrastructure usually survives; equity holders are the ones who eat the gap.

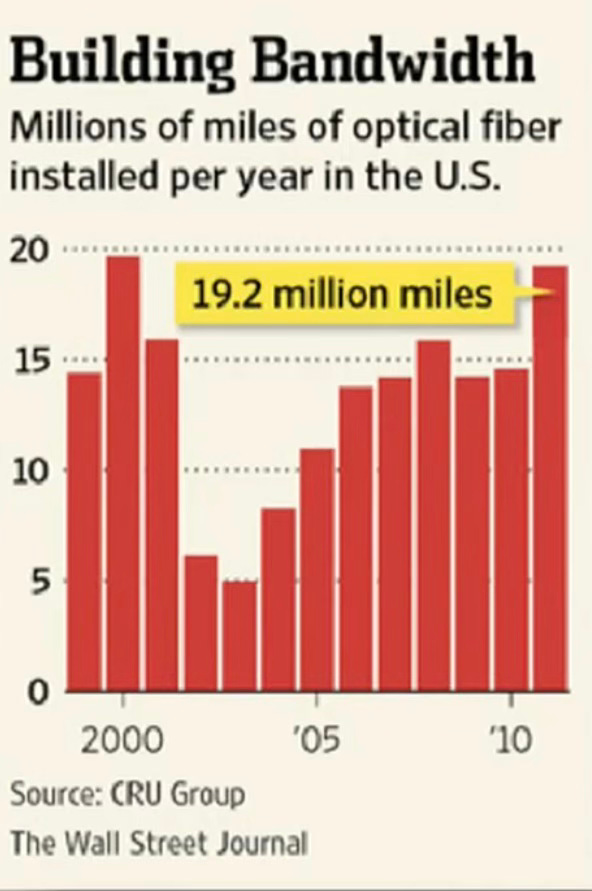

What made the fiber bubble lethal was speed. In 2000–2002 (most visibly 2001–2002), efficiency outpaced financial models. Capacity existed but didn’t need to be lit. Bandwidth prices fell on the order of –40% to –60% per year.

Global Crossing captured the sequence: revenue swaps peaked, debt reached the tens of billions, bankruptcy followed. Supply was built. Confidence was booked. Utilization lagged.

Fiber eventually proved enormously valuable—but much of the return arrived 10–15 years later with mobile and cloud demand. In the early 2000s, investors endured bankruptcies, restructurings, and assets sold for cents on the dollar.

Today, Dark Compute sits in that same gap—where technological inevitability collides with economic timing.

Now, investors today should be asking themselves, “Have we entered the AI Dark Compute phase?”

The 2026 Good Will Hunting Moment

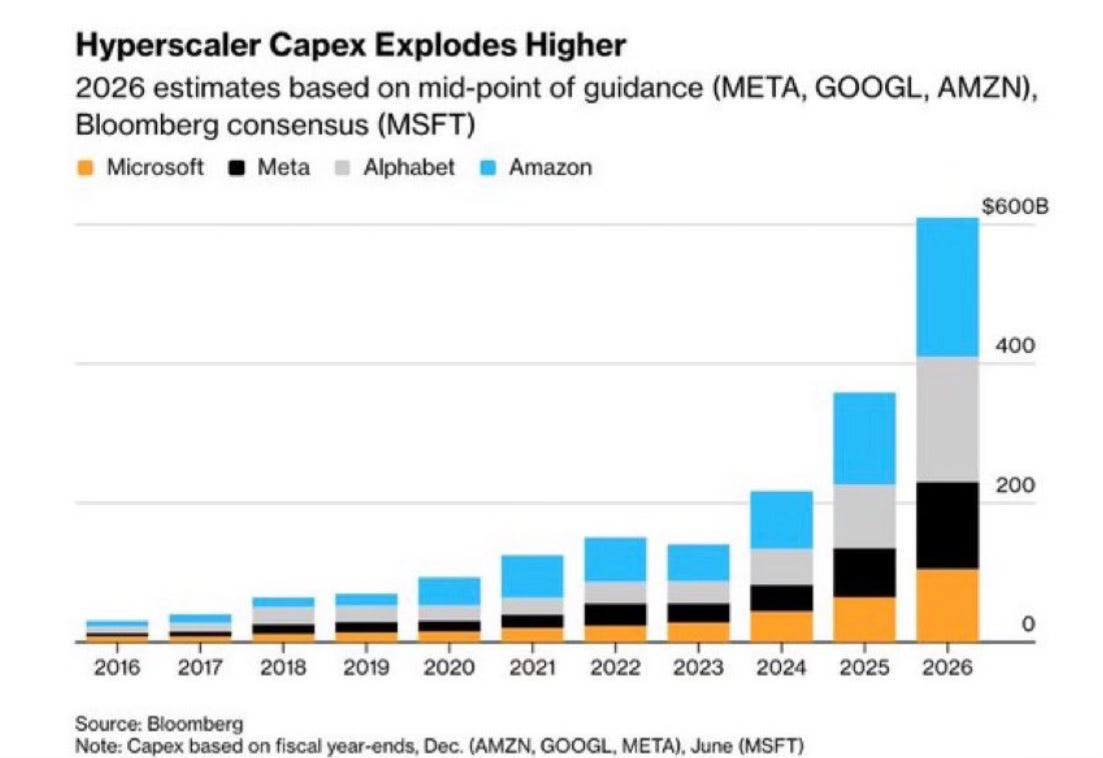

In 2026, hyperscalers are locking in a capex regime that’s gone structural: Axios pegs mid-point guidance around ~$610B for 2026, while Golden Coast Consultants estimates $660B–$690B across the five largest cloud/AI infrastructure players. Chief Market Strategist Greg Crennan ran the capex math, depreciation risk (more on that here ), and balance-sheet exposure in depth here: [AI Capex Report Link].

If capex spend is the pitch but efficiency is the reality, something has to break. The question isn’t demand—it’s monetization: where does Dark Compute hide in the buildout, and when do utilization, pricing, and returns reset to a lower-cost world?

Full Access Team Get The Answers To:

How Dark Compute is happening?

How quickly AI efficiency is already reshaping data-center ROI.

Where we are in the cycle—Scarcity → Efficiency Compression → Utilization Stress—and why timing changes the trade.

What Dark Compute does to the AI Capex investment thesis?

Which real-world constraints are already delaying ROI?

Whether Dark Compute is already here—and the signals that confirm it.