AMD Accounting Red Flags Continue

Trouble in the AI Chip Bubble

(Financial Risk Analysis – February 2025)

Wall Street has been here before—irrational exuberance, sky-high valuations, and companies leveraging financial smoke and mirrors to keep the dream alive.

At $119 per share, Advanced Micro Devices (NASDAQ: AMD) is priced for perfection, boasting a near-100 P/E ratio that assumes limitless AI-driven growth. But beneath the AI-fueled hype lies a more ominous truth: AMD’s latest earnings reveal a dangerous game of financial engineering, growing signs of business weakness, and a valuation detached from reality.

Investors should ask themselves: Are we witnessing another overhyped tech darling poised for a brutal correction?

1. The Accounting Tricks That Should Make You Nervous

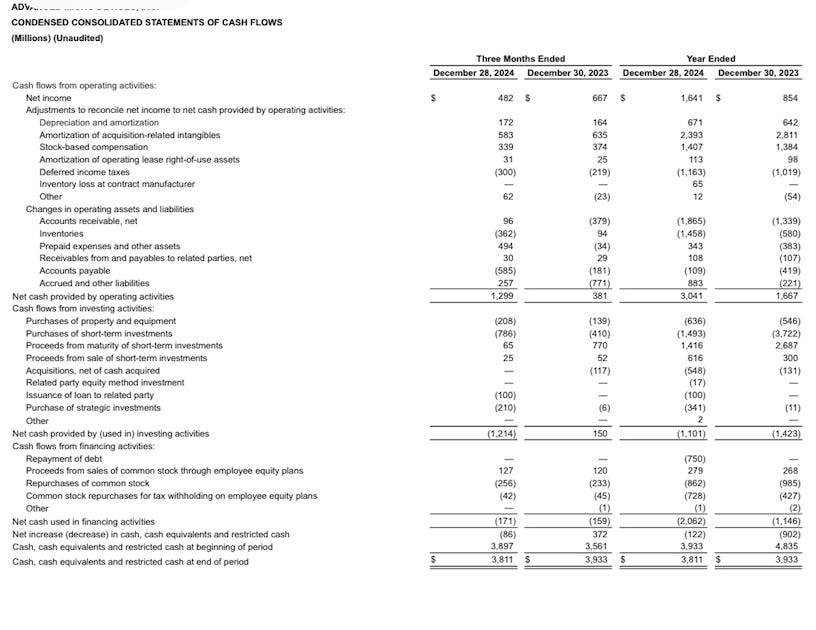

Red Flag #1: Rising Accounts Receivable – The Illusion of Growth

AMD’s accounts receivable have surged—this means the company is booking revenue before the cash actually arrives.

Classic corporate scandals have used this tactic to artificially inflate growth.

Meanwhile, cash flow from operations is declining, a textbook sign that revenue may be pulled forward to meet Wall Street’s expectations.

Red Flag #2: A Disturbing Inventory Build-Up – A Sales Slowdown?

AMD’s inventory levels have swelled, signaling that products—especially AI chips—aren’t moving as fast as expected.

Excess inventory leads to write-downs, which will eventually hammer future earnings.

If AMD’s MI300 AI chips were truly in high demand, why is inventory stacking up instead of flying off the shelves?

Red Flag #3: Deferred Revenue Shenanigans – Manipulating Earnings?

AMD appears to be shifting revenue recognition between quarters, a tactic that can create the illusion of steady growth.

If AI and data center demand were truly skyrocketing, AMD wouldn’t need to massage the numbers.

(AMD Financial Statement below)

Sign up for a full year and get 25% off.

Keep reading with a 7-day free trial

Subscribe to The Coastal Journal to keep reading this post and get 7 days of free access to the full post archives.