America's Housing Bubble 2.0

Introduction:

In the history of economic bubbles, few phenomena loom as large or cast as long a shadow as the housing bubble of 2007-2008. Its cataclysmic collapse reverberated throughout the global economy, leaving a trail of devastation in its wake. Yet, from the ashes emerged a semblance of recovery, nurtured by the deft interventions of the Federal Reserve in 2009 by doing something it has never done before, buying Mortgage Backed Securities.

However, what began as a phoenix rising from the ashes now teeters on the brink of annihilation. The real estate market, once rejuvenated by the Federal Reserve's measures through quantitive easing (buying of government mortgage backed securities), now faces an impending cataclysm of unprecedented proportions. The intricate web of factors contributing to this looming disaster warrants a meticulous examination.

Historical Context of Housing Bubble 1.0:

America's housing bubble 1.0 can be traced back to the early 2000s, a period characterized by relaxed lending standards, widespread speculation, and the proliferation of complex mortgage instruments such as adjustable rate mortgages, credit default swaps, synthetic collateralized debt obligations, and the low interest rates set by the Federal Reserve in 2001. This confluence of factors led to a dramatic escalation in housing prices, fostering a deceptive sense of economic well-being and triggering a speculative frenzy that was inherently unsustainable.

The bubble's eventual burst in 2008 resulted in significant economic turmoil, exacerbated by rising interest rates and the inability of individuals to refinance their debts, leading to defaults and subsequent failures of mortgage-backed securities (MBS) and collateralized debt obligations (CDOs). This tumult culminated in the most severe financial crisis since the Great Depression, marked by soaring unemployment rates, widespread corporate bankruptcies including banks like Lehman Brothers, and a sharp decline in stock prices of approximately 50% on major indices.

To alleviate this crisis, in March 2009, the Federal Reserve embarked on an unknown and untested strategy aimed at reviving the struggling real estate market. This strategy, known as Quantitative Easing (QE), involved the central bank's unprecedented purchase of US government securities, particularly mortgage-backed securities, to inject liquidity into the market and artificially depress interest rates to historically low levels. The objective was to stimulate demand, prop up real estate prices, and reignite economic activity. This intervention heralded a new era characterized by resurgent real estate values, robust demand, and a rebirth of speculative activity in the housing market. However, the long-term sustainability and potential risks associated with this intervention remain subjects of ongoing debate and scrutiny among economists.

Inflating of Housing Bubble 2.0:

Today's housing bubble 2.0 was inadvertently inflated during the upheaval of the COVID-19 pandemic. In 2020, as the pandemic wreaked havoc across the nation, the Federal Reserve once again deployed its monetary tools, injecting trillions of dollars into the market through the purchase of nearly $3 trillion worth of Mortgage-Backed Securities (MBS), which accounted for nearly half of all MBS available. As the country returned to normal activity in 2021, the Federal Reserve persisted with its assertive asset acquisitions under the umbrella of Quantitative Easing (QE), with a steadfast aim of maintaining historically low interest rates.

The repercussions of this substantial monetary stimulus were swift and far-reaching. As 30-year mortgage rates plunged to unprecedented depths, hovering around 2.5% and reaching their bottom in 2021—a level unseen in recorded history extending back to the Roman Empire—the housing market experienced an explosive surge in demand. The allure of exceptionally affordable monthly mortgage payments enticed a flood of eager buyers into the market, propelling real estate prices to unprecedented heights.

This surge in demand and subsequent price escalation underscores the powerful influence that low interest rates wield in stimulating economic activity, particularly in the housing sector. By significantly reducing the cost of borrowing, low interest rates incentivize prospective homebuyers to enter the market, thereby increasing competition and driving up prices. However, it is crucial to note that while low interest rates can stimulate demand and boost asset prices, they can also contribute to the formation of asset bubbles if not carefully monitored and managed.

Price Dynamics:

As if in a cruel twist of fate, the exorbitant prices that once defined the market's feverish euphoria now stand as testaments to its impending doom.

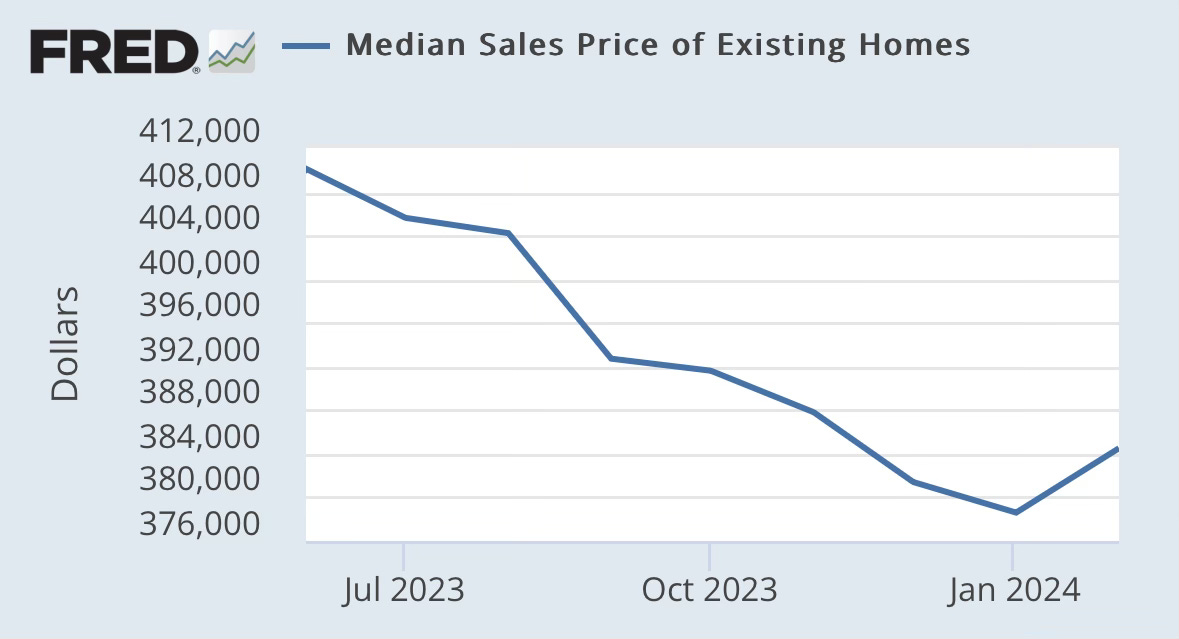

The toll on housing prices is staggering. According to an old saying, the cure for higher prices is higher prices. Median sale prices have declined from their 2022-2023 highs as the Federal Reserve stopped buying MBS in 2022, resulting in interest rates soaring to as high as 8%, with current rates hovering at 7%.

Median sale prices for existing homes dropped from the high of $416,00 to $384,500 (a decline of -7.5% from the peak).

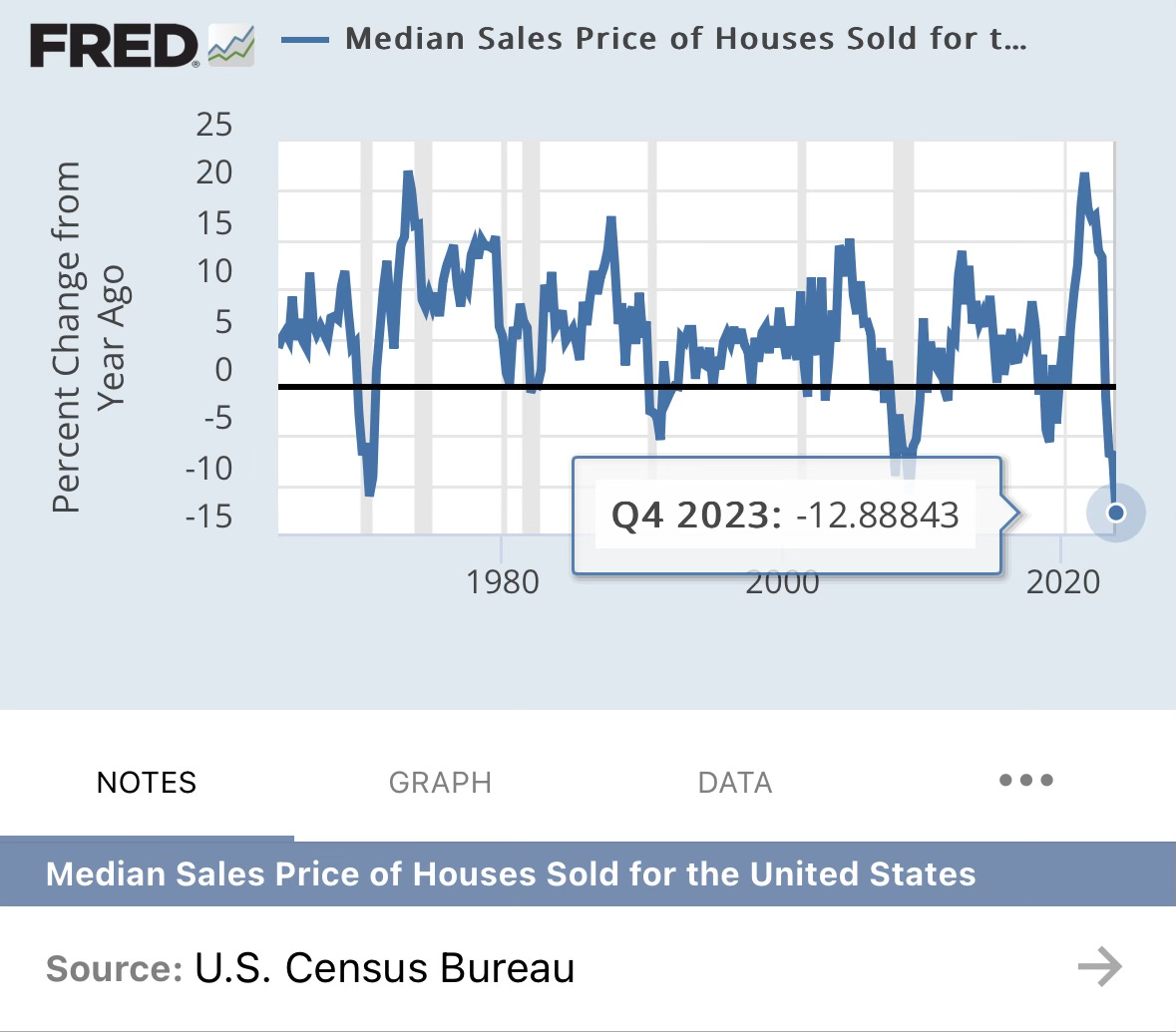

Similarly, all median sales prices has come declined by 13%, the largest year over year decline recorded. These declines, unprecedented in their magnitude, serve as leading indicators of economic distress, surpassing even the downturn witnessed in the aftermath of the 2008 crisis.

Current Conditions of Housing Bubble 2.0 (March 2024):

As we analyze the current data and indicators, a somber narrative unfolds, casting a shadow of impending decline over the real estate horizon. At the forefront of this narrative are 30-year mortgage rates, hovering near a daunting 24-year high, surpassing 7%. This sharp increase in borrowing costs serves as a stark warning sign, exerting immense pressure on the housing market by stifling demand.

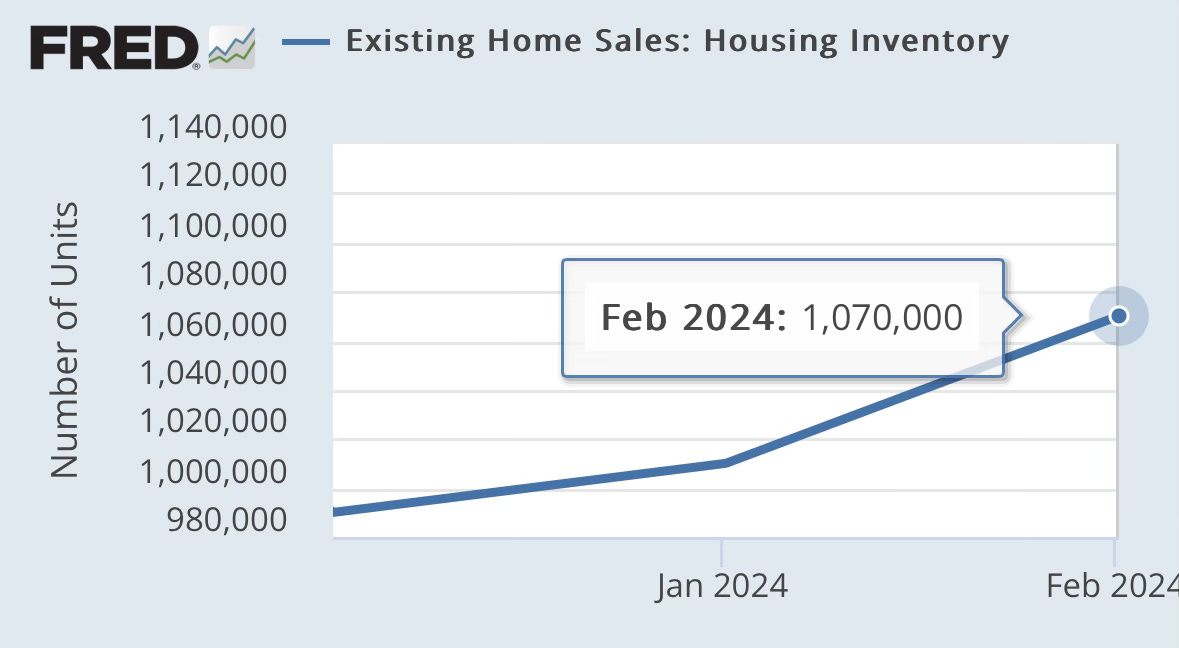

The surge in mortgage rates has triggered a frenzied rush among property owners to sell, resulting in a projected 40% increase in housing inventory by July, building upon a 10.3% rise in the first few months of the year, totaling 1.07 million houses for sale. This influx of available homes is propelled by both the relentless climb of mortgage rates and the urgency felt by sellers to offload their properties before market conditions deteriorate further.

February's statistics offer no respite, showcasing a continued decline in the number of unsold homes and a persistent rise in homes actively for sale. This trend, now extending into a fourth consecutive month, paints a grim trajectory for the market.

Amidst this turmoil, a sense of desperation permeates as a significant portion of homes—30.5%—slash their prices, reflecting the market's rapid descent. Nationally, 5.5% of homes have witnessed price drops, marking the highest share in any February since at least 2015. Against this backdrop, pending sales continue their downward trajectory, further signaling the impending downturn of the market.

Are we in a Real Estate Bubble 2.0?

In the film "The Big Short," a skeptical investor reflects on Michael Burry's decision to short the housing market, noting, "No one knows it's a bubble, that's what makes it a bubble." This sentiment underscores the inherent challenge of identifying and acknowledging financial bubbles in real-time. To dive into this question further, let us examine the dynamics of regional housing markets and their potential bubble-like characteristics.

The tendency to downplay leading indicators or overlook warnings of bubbles often stems from a desire to maintain a positive narrative about the economy. This reluctance can lead to dismissing signals that might burst the bubble or contradict mainstream perceptions of economic health. At the peak of Housing bubble 1.0, former Federal Reserve Chair Alan Greenspan acknowledged the presence of a housing bubble, but downplayed its potential impact on the broader economy. In the interview, Greenspan suggested that housing bubbles are regional and defaults are rare.

However, historical evidence has shown that housing bubbles can indeed have far-reaching consequences beyond regional borders. Therefore, it is essential to critically examine regional housing markets within the broader economic context. By doing so, we can gain insights into potential bubbles and assess systemic risks.

Adopting a vigilant approach that incorporates data-driven analysis and economic theory allows us to better understand market dynamics, identify emerging risks, and make informed decisions to promote economic stability and resilience.

Austin: Silicon Hills

Austin, famously dubbed Silicon Hills, exhibited remarkable resilience during the housing bubble 1.0 compared to the broader American real estate market. However, subsequent developments, especially post-2009, have painted a different picture.

The Federal Reserve's extensive quantitative easing (QE) measures, coupled with business-friendly tax incentives, triggered a massive influx of California-based technology companies into Austin. This migration, bolstered by Austin's favorable climate and tax environment, fueled a significant real estate boom. The culmination of this boom coincided with the widespread adoption of work-from-home policies in 2021, further intensifying demand for Austin's housing market.

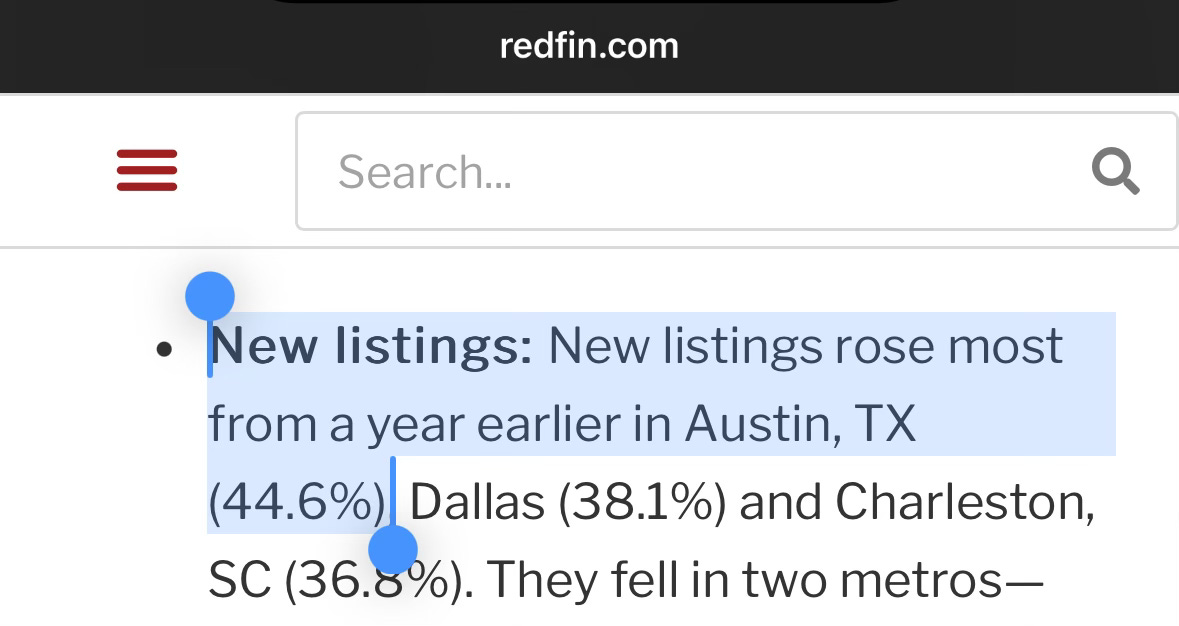

Despite these favorable conditions, all booms inevitably face a bust phase. Austin experienced a surge in new housing supply over the past decade, leading to an oversupply scenario. According to Moody's data, Austin's home prices are currently 35% higher than what the city's economic fundamentals would support. Also, supply is sky rocketing in 2024 as new listings are up an insane 44%. This stark disparity between prices and underlying economic trends is a cause for concern.

To put current prices into perspective, Austin's per capita income rose by 23% between 2020 and 2022. However, during the same period, home prices skyrocketed by 100%. Such rapid price escalation, outpacing income growth, transforms houses from assets into burdensome debts due to inflationary pressures.

The downturn is not limited to homeownership; apartment prices are also witnessing a decline. Austin has experienced a surge in apartment construction, surpassing other cities in America. This steep increase in available shelter supply is outpacing housing demand, leading to price declines in both home prices (by 20%) and renting (by 7%).

Moreover, the rising unemployment rate in Texas, up by 63% since 2022, further exacerbates the housing market challenges. Increased unemployment reduces the pool of potential homebuyers while potentially prompting current homeowners to consider selling to generate much-needed cash.

Silicon Valley AI Frenzy is deflating Housing:

San Francisco, renowned as Silicon Valley, has emerged as the epicenter of the AI revolution in 2024. The meteoric rise of tech companies' stock prices, reminiscent of the Tech bubble 1.0 in 2000 and the market valuations of 1929, has garnered significant attention from the media, often dubbing these companies as the MAG7, Magnificent 7, AI 5, or the FAB 4, depending on market fluctuations that week. This euphoria has led many to believe that these companies are driving a booming economy. However, a closer look at the economic data in Silicon Valley paints a more nuanced picture.

Despite the soaring stock prices and market hype, Silicon Valley is grappling with rising unemployment rates, among the fastest in the nation. Concurrently, real estate prices are experiencing significant declines down as much as 30% in some parts of the value as supply of housing inventory jump double-digits for the first time in 19 months in 2024, comparable to some of the largest drops since their peak. Another impact on all of California’s real estate is that continued claims of unemployment, up about 72% since 2022.

This data raises a critical question: why is the AI capital of the world, seemingly thriving in terms of stock market valuations, witnessing a drastic drop in real estate prices?

Other Regionals, The Sunbelt Cities:

On the other hand, the Sunbelt cities, including Phoenix, Las Vegas, Dallas, and various cities in Florida, experienced a massive surge of demand due to lower interest rates and the work-from-home trend. These cities, previously characterized by normal housing demand, saw an influx of residents from regions like New York, California, and Washington, seeking more affordable living and remote work opportunities.

Also, the rapid rise in prices and speculation in the Sunbelt cities was fueled by people purchasing properties for Airbnb management or other rental purposes. However, as inflation erodes purchasing power, Airbnb properties are witnessing declines, with individuals opting for more traditional hotel accommodations or choosing not to travel altogether.

In 2024, the Sunbelt cities are facing higher unemployment rates as well as a surge in housing supply, leading to price declines. This combination of factors highlights the complex interplay between economic trends, housing markets, and consumer behavior in different regions, underscoring the need for a nuanced understanding of these dynamics to navigate the evolving economic landscape effectively.

(To find out more about what is popping America’s Housing Bubble 2.0, subscribe to the Coastal Journal today. You will receive more in depth economic white papers in the future, as well as free weekly newsletters on the latest economic news.)

Keep reading with a 7-day free trial

Subscribe to The Coastal Journal to keep reading this post and get 7 days of free access to the full post archives.