Bank Earnings Are As Cold As Ice

Part I: JPMorgan, Citi and Wells Fargo – The Forensic Breakdown

The Ice Age of Inflation — And What the CPI Report Isn’t Telling You

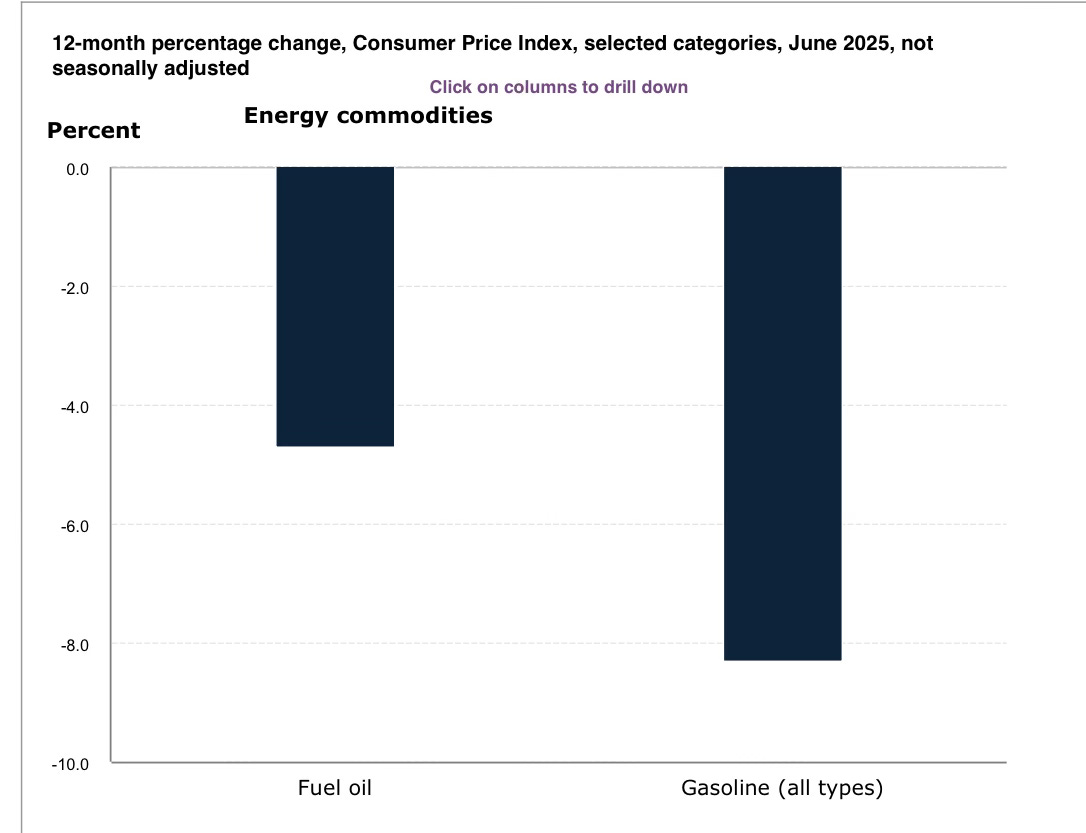

Before diving into the bank earnings, we need to talk about the real financial freeze hitting American households: inflation. According to the latest data, the headline CPI number came in at 2.7%, but that’s a number distorted by a single volatile factor—gasoline prices. With gas down -8% year-over-year, it’s dragging the overall average lower.

Strip that out, and the true story is very different.

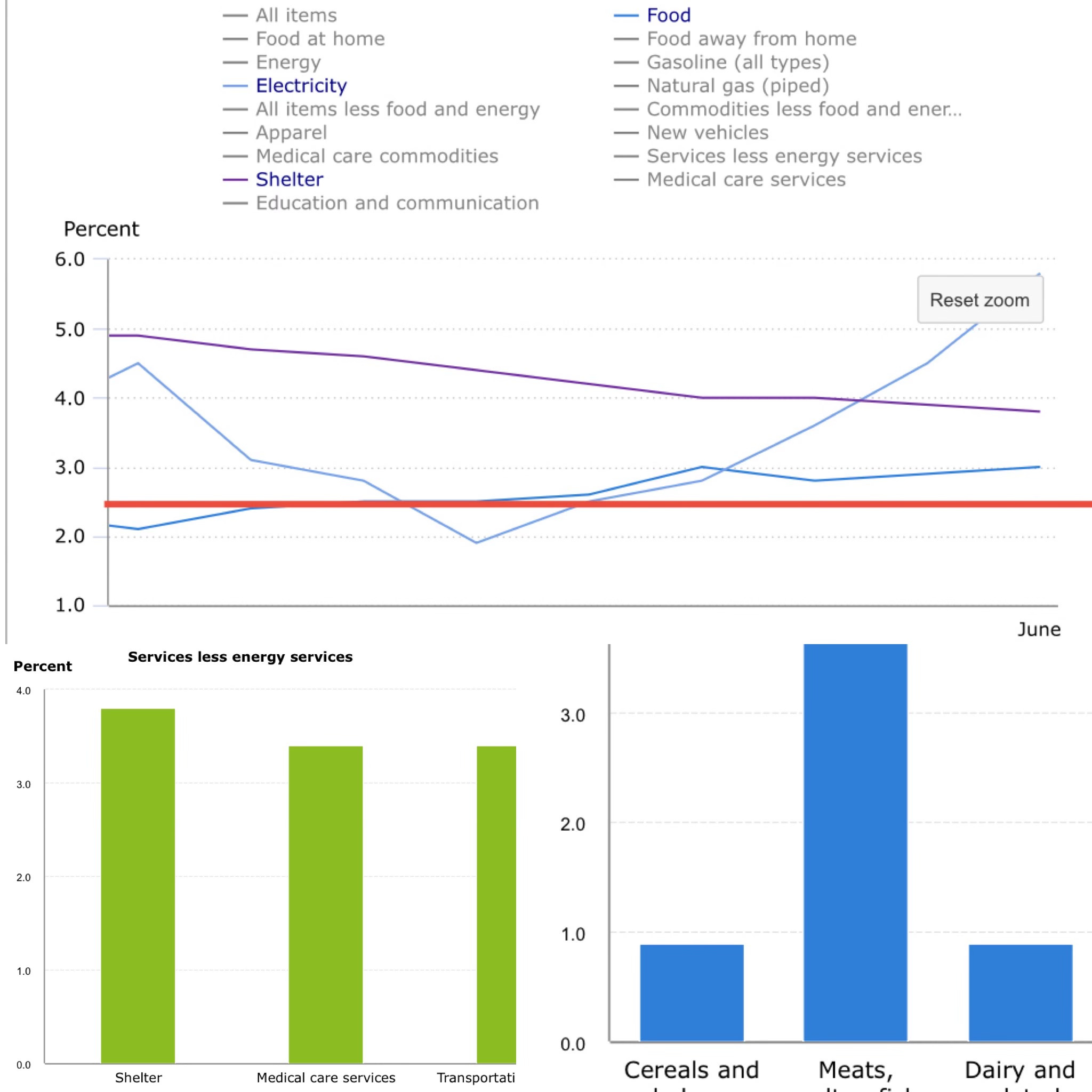

Shelter remains painfully expensive, climbing 4% over the last 12 months. Medical services and transportation are both up 3.5%. Food? Whether at home or eating out, prices are still rising at a pace between 4–5%. Electricity has surged nearly 6%—an essential no one can skip. These aren’t luxuries. They’re non-negotiable, everyday expenses. And they keep climbing.

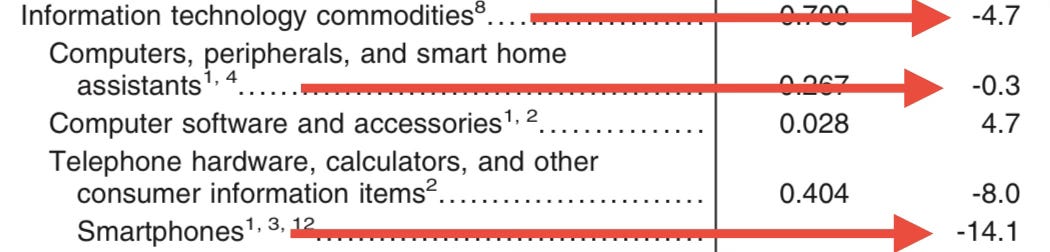

Meanwhile, the items that are falling—TVs, smartphones, clothing.

These are the sectors most affected by tariffs, and yet, their prices are going down, not up. The idea that tariffs are driving inflation falls apart when you look at the data. What’s really happening is that the core, domestic cost structure—housing, healthcare, food, and power—is still climbing while the things Americans don’t need as much are dropping in price. Thats as cold as ice!

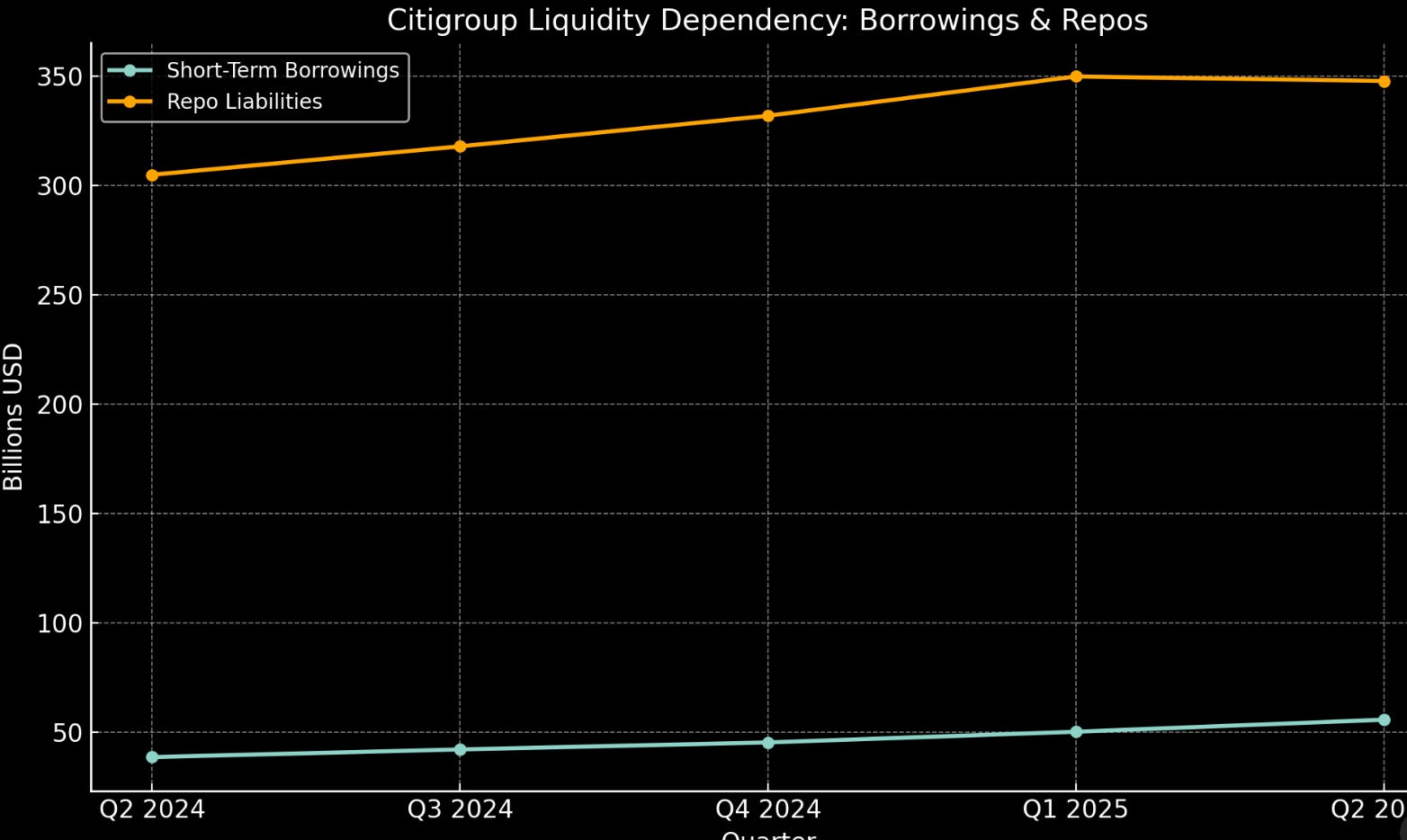

Citi Short Term Borrowing Soars

Citigroup’s Q2 2025 earnings reveal a serious liquidity warning. Short-term borrowings surged to $55.6 billion, up 44% year-over-year—an unusual spike that suggests Citi is relying heavily on external debt markets rather than stable deposits to fund operations.

More alarming, Citi still holds $347.9 billion in repo liabilities, up 14% from last year. This means a large portion of its funding is short-duration, market-sensitive, and must be rolled over constantly. If repo markets tighten or rates spike, Citi could face serious funding pressure.

There’s no hidden accounting trick—everything’s on balance sheet—but the scale and direction of the borrowing tells the story: Citigroup doesn’t have the liquidity cushion it should, and it’s quietly depending on fragile capital markets to stay upright. That’s a systemic red flag.

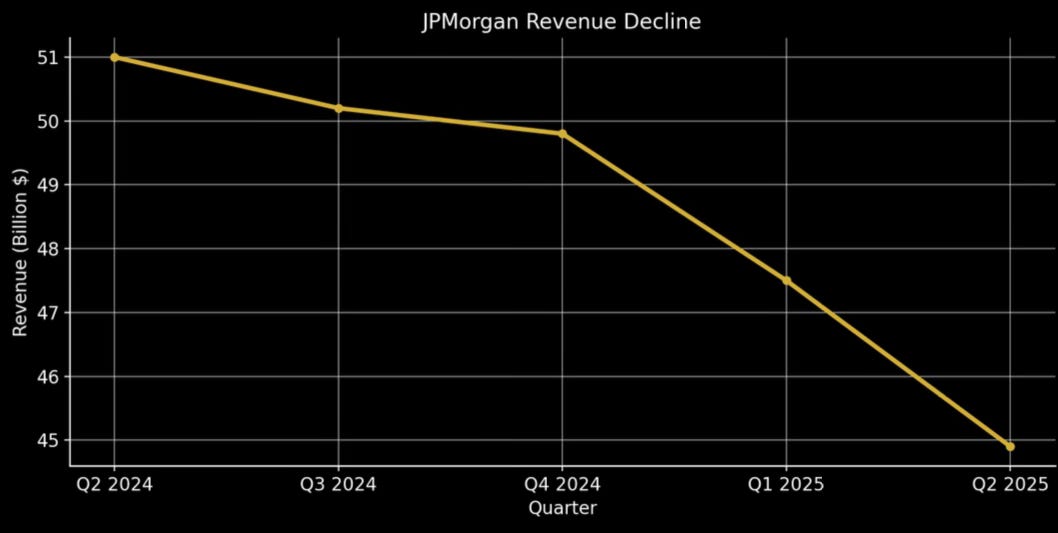

JPMorgan: A Cold Reality Behind the Curtain

JPMorgan's Q2 2025 earnings are being spun by Wall Street as a “BEAT,” but that’s nothing more than theater. The truth is that Wall Street slashed estimates beforehand, setting the bar so low even a flat quarter could clear it. But this quarter wasn't flat—it was a step backward.

Net revenues fell -11.9% year-over-year to $44.9 billion.

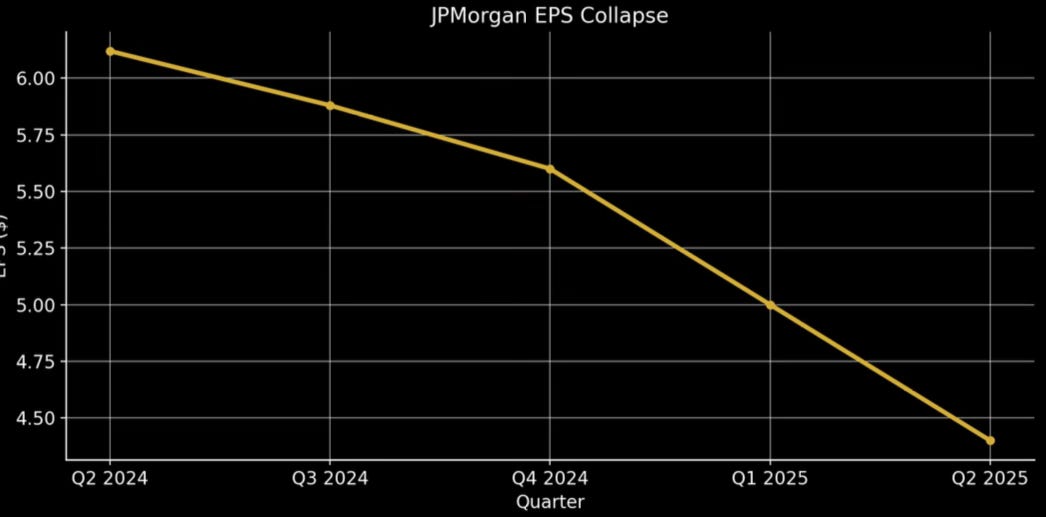

EPS collapsed from $6.12 in Q2 2024 to $4.40 in Q2 2025. That’s a -28% drop in per-share earnings, yet the stock was bid higher. The narrative pushed is that “JPM is managing the downturn well,” but there’s no sugarcoating the numbers: profitability is deteriorating.

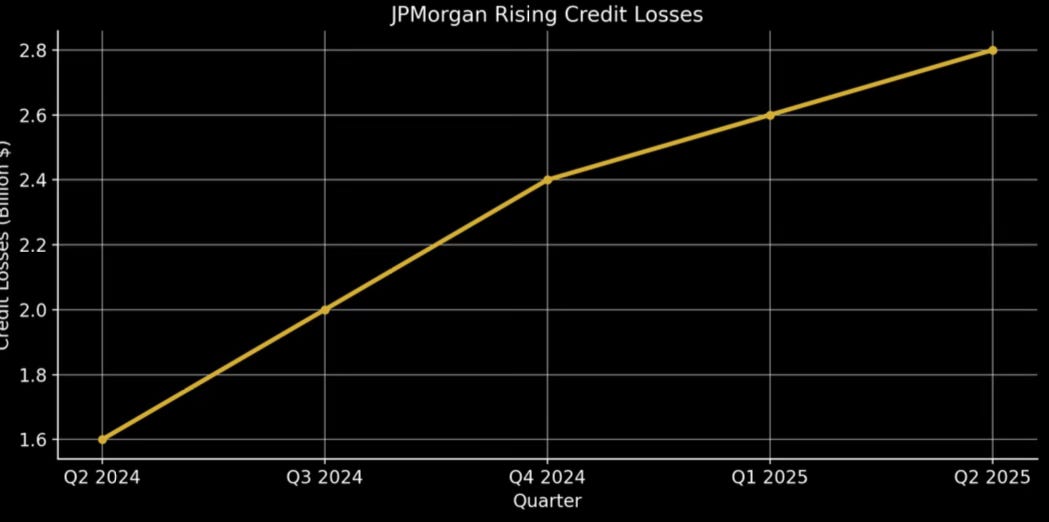

More concerning, JPM recorded $2.8 billion in credit losses, a sharp YoY increase, indicating that loan quality is weakening. This isn’t happening in isolation—credit card charge-offs are at 3.4%, up significantly and signaling consumer strain. Reserve builds are accelerating, not shrinking. Management is quietly admitting the consumer is faltering, even if the headlines won’t.

🔒 FULL ACCESS COASTAL JOURNAL BELOW 🔒

What you unlock as a paid subscriber:

Full forensic earnings breakdowns for JPMorgan & Wells Fargo

Detailed accounting Red Flags Wells Fargo Repo Surge 34% a $188 BILLION Spike (WARNING)

Golden Coast’s tactical options strategies (including JPM & WFC put setups)

Custom risk maps on credit losses and repo spikes (liquidity problems)

Keep reading with a 7-day free trial

Subscribe to The Coastal Journal to keep reading this post and get 7 days of free access to the full post archives.