NVIDIA Earnings : A Financial Detective’s Case

The Case of the Disappearing GAAP & More

The financial stage is set, and the spotlight shines brightly on NVIDIA, the darling of Wall Street. In a move as calculated as a grandmaster’s chess play, NVIDIA has opted to file an 8-K instead of the traditional 10-Q, redirecting attention to its Non-GAAP earnings and away from the more sobering realities of GAAP metrics. This is no ordinary earnings report—it’s a masterclass in financial storytelling.

Sherlock Holmes once said, “It is a capital mistake to theorize before one has data,” yet here, the data itself weaves a tale of accounting acrobatics. Investors, like Watson’s wife seeking answers from the great detective, are left pondering: “What can you tell about me?” The clues lie buried in the balance sheets, and the game is on. Will this be a triumph of innovation or a cautionary tale of financial engineering?

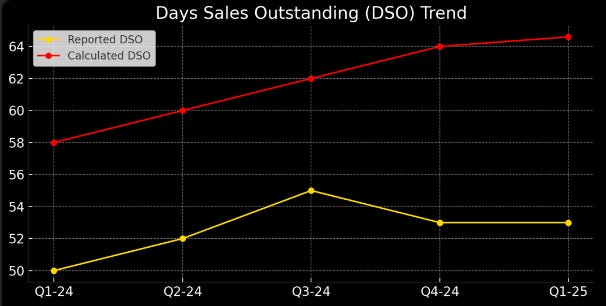

One glaring issue lies in Days Sales Outstanding (DSO). NVIDIA reports DSO at 53 days, but a closer examination of the numbers reveals the real figure to be approximately 64.6 days. This discrepancy suggests the company may be selectively excluding certain receivables or using quarterly revenue figures to understate the true time it takes to collect payments. Such a maneuver could mislead investors into believing the company is more efficient at managing its receivables than it actually is.

Another concerning red flag is Inventory Days Sales Outstanding (DSI). NVIDIA reports DSI at 86 days, yet the true calculation places it at 112.8 days. This suggests that NVIDIA may be inflating its inventory turnover rate, potentially masking sluggish demand or slower-than-reported sales cycles. Overstating efficiency in inventory management can create an illusion of robust operational performance while hiding potential risks of obsolescence or overproduction.

Keep reading with a 7-day free trial

Subscribe to The Coastal Journal to keep reading this post and get 7 days of free access to the full post archives.