Economic Reality: We Want the Truth About Interest Rates & Inflation

We Can Handle The Truth

Echoing Tom Cruise's memorable demand in 'A Few Good Men,' 'I want the truth!', today's Americans are clamoring for answers regarding inflation, interest rates, and the economy, demanding nothing less than the unvarnished truth.

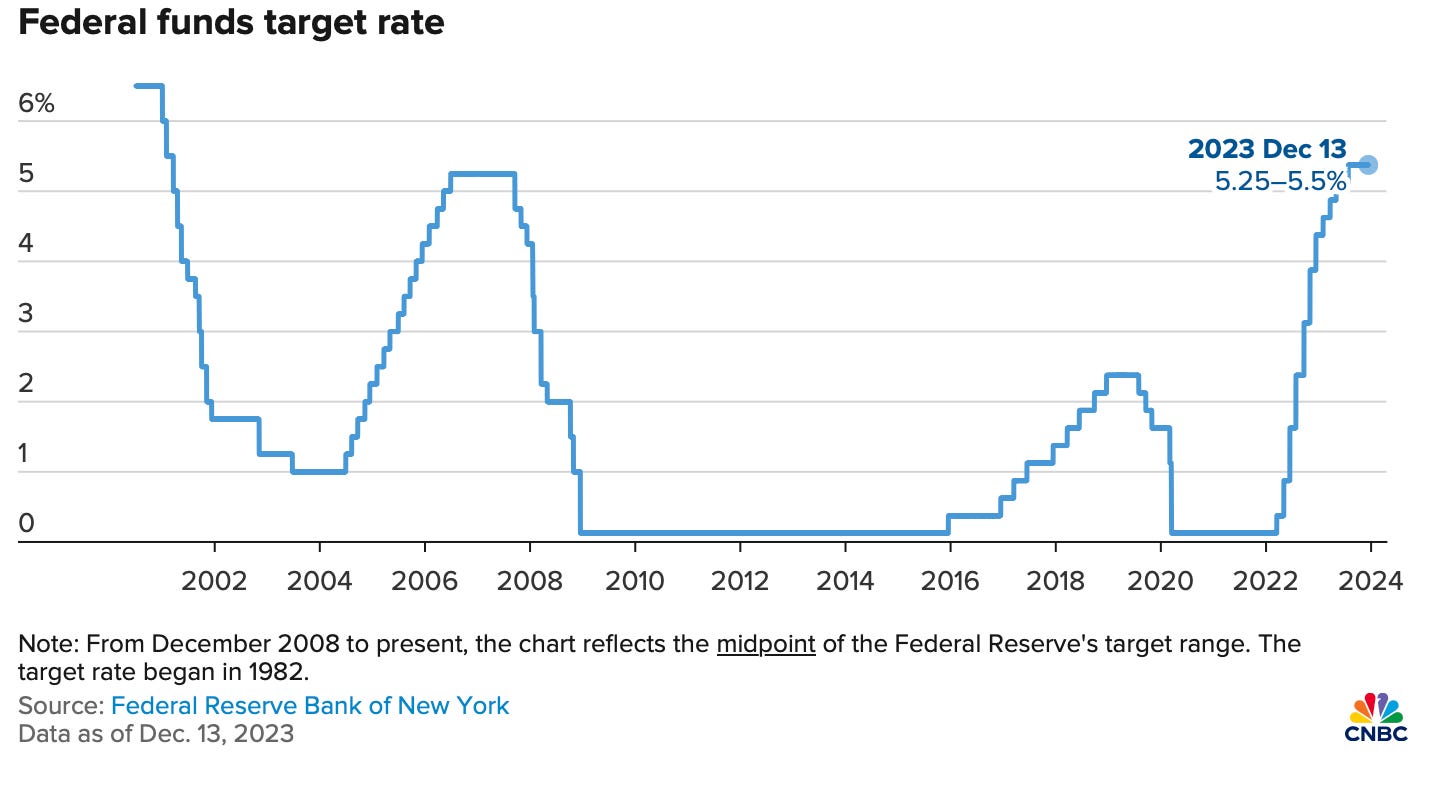

This demand resonates today through out America as we scrutinize interest rates in the global economy. With interest rates currently at the highest they have been in the past 24 years, many people burdened with debt are hoping for a decrease soon. However, the truth about interest rates and their impact on inflation is complex and requires careful analysis.

The narrative that current interest rates around 5% are stimulative for the economy is misleading. In reality, these rates are insufficient to effectively control inflation. Let's break down the data: the latest Bureau of Labor Statistics (BLS) report shows a year-over-year inflation rate of 3.6%. With interest rates around 5%, many economists state that real rates (interest rates minus inflation) are positive at 1.4%. However, this does not tell the full story.

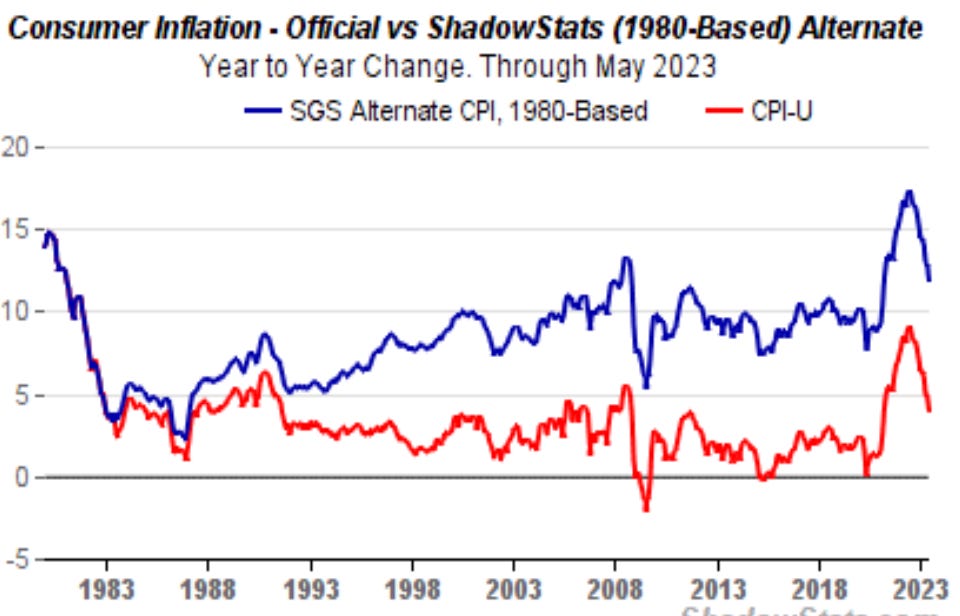

The BLS report is heavily skewed by year-over-year increases in gas and shelter costs, based on Owners' Equivalent Rent (OER). Actual housing, monthly mortgage payment and rent prices are not directly reflected in the index. According to Shadowstats, a website known for offering alternative economic data using methodologies from past decades, the inflation rate calculated using 1980s methodologies is significantly higher than the official rate, often cited at around 10% or more. This discrepancy highlights the impact of methodological changes over time.

Using these higher estimates, the real-world inflation rate is far more critical than the reported figures. When calculating real rates with this higher inflation, we find them to be alarmingly negative. With inflation at 10% and interest rates at 5%, real interest rates plunge to -5%. This means the purchasing power of money is eroding over time, with lenders and investors effectively losing value, while borrowers, including the US Government, benefit from repaying loans with devalued currency.

To further illustrate the dire impact of inflation, let's compare the high-inflation period of the 1980s with today. Back then, with interest rates around 20%, someone with $20,000 in savings could earn a substantial $4,000 in risk-free interest income. Fast-forward to 2024: to earn that same $4,000 at a 5% interest rate, one would now need a staggering $90,000, showcasing the severe erosion of purchasing power over time. For a typical individual to achieve a $4,000 return adjusted for inflation in 2024 they would need to earn about $16,000 a year, meaning interest rates would need to skyrocket to 16% for the same type of return.

Today, the average American has about $65,000 in personal savings. At a 5% interest rate, this would yield only $3,000 after 12 months. However, when adjusting for the reported inflation rate of 3.6%, the real return shrinks to a meager $1,000. Accounting for the real-world inflation rate, the return isn't just small—it's a guaranteed loss. This starkly contrasts the supposed stimulative effect, highlighting how savers are punished in this high-inflation environment, with their hard-earned money losing value faster than they can earn it.

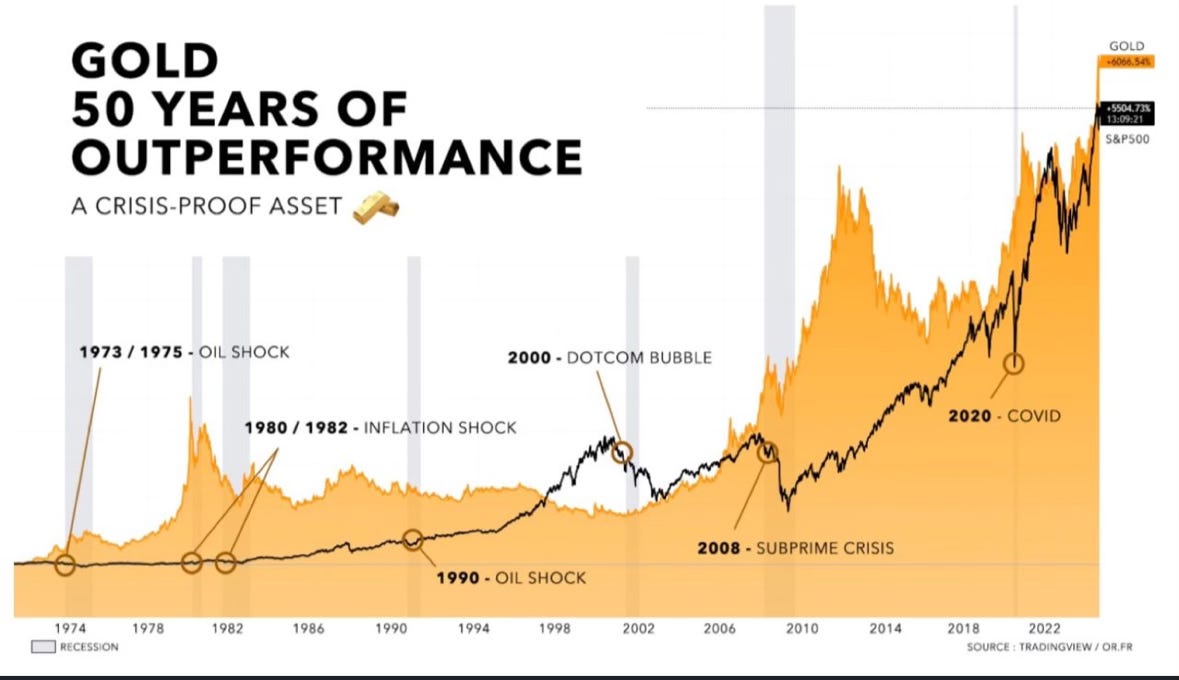

This scenario, where inflation surpasses interest rates, is devastating for savers and lenders, as the real value of their money diminishes faster than any nominal returns. Conversely, it incentivizes borrowing and investing in tangible assets like real estate, precious metals, stocks, and even speculative investments like cryptocurrencies.

As a result of these negative real rates, investors are fleeing the dollar, triggering a frenzy of speculation and driving stocks to record-high valuations, particularly within the Tech AI Bubble. This investor behavior has also spurred a rush to the world's ultimate safe haven asset, gold, which has surged by 18% in 2024, reaffirming its status as the best hedge against inflation since the Roman Empire. (For additional information on the Roman Empire check out a previous article here: When In Rome )

Silver, another precious metal with a trillion-dollar market, has outperformed even the speculative mania of the AI-driven Tech Bubble 2.0, skyrocketing by 35% in 2024 compared to the tech sector's 11% gain as of May 21, 2024. Additionally, this environment has reignited massive flows of billions of dollars into highly speculative crypto pyramid schemes, exacerbating the financial turbulence.

Consumers are feeling the pain as interest rates aren’t high enough to offset high inflation, leading to a record high in credit card debt at $1.1 trillion. Credit card delinquencies are soaring, approaching levels seen during the Great Financial Crisis of 2008. Simultaneously, the personal savings rate has hit a new record low, indicating that as real wages fail to keep pace with the standard of living, Americans are relying more on credit card debt and depleting their savings to get by each month.

Even market leaders are expressing concern. Jamie Dimon, CEO of JP Morgan, has stated that buying his stock at $200 a share with a "2 times tangible book value is a mistake," reflecting how overvalued assets have become in this speculative environment. (For Clip of Jamie Dimon Click Here )

As former Federal Reserve Chairman Paul Volcker stated, interest rates represent the cost of capital, not the quantity of money in circulation. With the current money supply standing at $21 trillion, higher real interest rates are needed to incentivize saving and curb inflationary pressures.

You want the truth, but many pundits suggest you can't handle the truth. The truth is that current interest rate levels are not high enough to effectively combat inflation, causing a stagflation environment and for more information on Stagflation check out this previous post (Hotel Stagflation ). Until policymakers acknowledge this reality and take decisive action, the economy will continue to face inflationary challenges.

Great article

Thank you!