Nvidia & OpenAI: The $100B Round-Tripping Mirage

Nvidia’s $100B Letter of Intent with OpenAI grabs headlines — but will the promises be delivered?

Nvidia and OpenAI’s $100B Letter of Intent sparks AI euphoria today in the Stockmarket, fueling a cycle of manufactured AI demand through round-tripping deals, receivables bloat, and more — here’s what investors need to know.

“You spin my head right round, right round…” was Flo Rida’s club anthem from 2009 could easily serve as the soundtrack for Nvidia’s financial ballet in 2025.

The company has mastered the art of turning AI hype into a perpetual motion machine: selling chips to partners, backstopping their unused capacity, and layering on grand promises of future investments. To the casual investor, it looks like boundless demand. To anyone who has studied past financial blowups, it looks uncomfortably familiar.

Nvidia, OpenAI, and CoreWeave are carrying on a financial tradition with a familiar playbook. In the late 1990s, telecom firms inflated growth by trading bandwidth back and forth, recording sales that never touched a real customer. Enron then took the scheme further, round-tripping energy contracts through shell entities it secretly controlled, generating dazzling revenue on paper while no real cash flowed through the system. These episodes ended the same way: with investors realizing the “growth” was just an illusion built on accounting gimmicks.

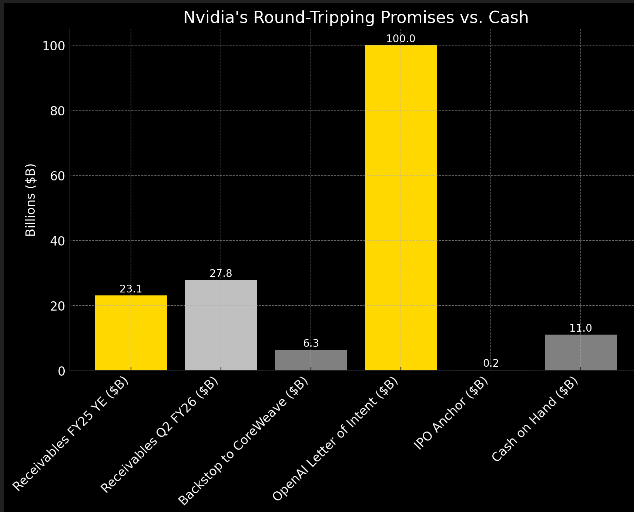

The echoes today are hard to miss. Nvidia sells GPUs to CoreWeave, then guarantees CoreWeave’s unused capacity through a $6.3 billion backstop that runs until 2032 (last weeks news).

When CoreWeave’s IPO faltered, Nvidia stepped in with a $250 million anchor order to keep it alive. If Nvidia didn’t do that, it would have caused panic in the AI bubble rising questions on how strong demand really is? Now, Nvidia has pledged $100 billion to OpenAI — a company that is simultaneously one of its largest customers.

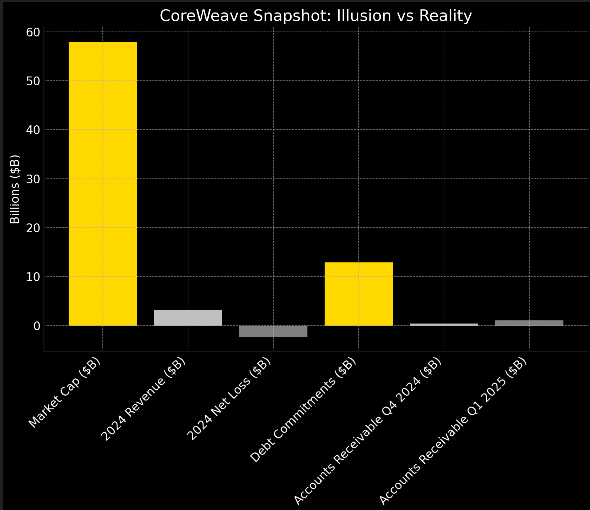

On paper, the results glitter like a Vegas marquee. CoreWeave’s valuation has rocketed to nearly $58 billion even as it bled -$2.3 billion in losses. Nvidia, meanwhile, reported receivables swelling to $27.8 billion in just six months — profits booked, but cash still waiting to arrive. Strip away the shine, and the pattern is all too familiar: revenues without liquidity, promises piled higher than the balance sheet can bear, and round-tripping demand cycles masquerading as growth.

At the center of this storm sits Nvidia — a company that has become the poster child for the AI Bubble, yet whose books carry the same fingerprints left behind by past bubbles. Investors may feel the rush of the ride from the stock today, but history suggests these round and round spin cycles always end the same way: not in deliverance, but in dizziness, as the music stops and the promises come due.

For Full Corweave Accounting Breakdowns ( CLICK HERE )

For Full Nvidia Accounting Breakdown (CLICK HERE )

Want to know if Nvidia’s promises to OpenAI are real demand or just financial spin?

Curious how CoreWeave’s IPO lifeline ties directly back to Nvidia’s balance sheet?

Ready to see what the Nvidia options market is signaling for the rest of the year?

CoreWeave: The $58B House of Receivables

CoreWeave tells the same story as Nvidia, only in miniature — and in some ways, even starker. In the first quarter of 2025…..

Keep reading with a 7-day free trial

Subscribe to The Coastal Journal to keep reading this post and get 7 days of free access to the full post archives.