Nvidia Earnings: What’s Inside the Box (8k)?

Earnings beat or Earning Miss?

"WHAT'S IN THE BOX?!" — Detective David Mills, Se7en

There are moments in film that echo into real life—and in the financial world, none cut deeper than the final, devastating crescendo of David Fincher’s Se7en. Picture this: not a sun-blasted field, but the fluorescent void of CNBC’s live ticker. Brad Pitt isn’t a detective anymore—he’s the investor, screaming as the box is pried open, desperate to know if the hope he bet on is about to become horror.

And Nvidia’s latest 8k? That’s the box.

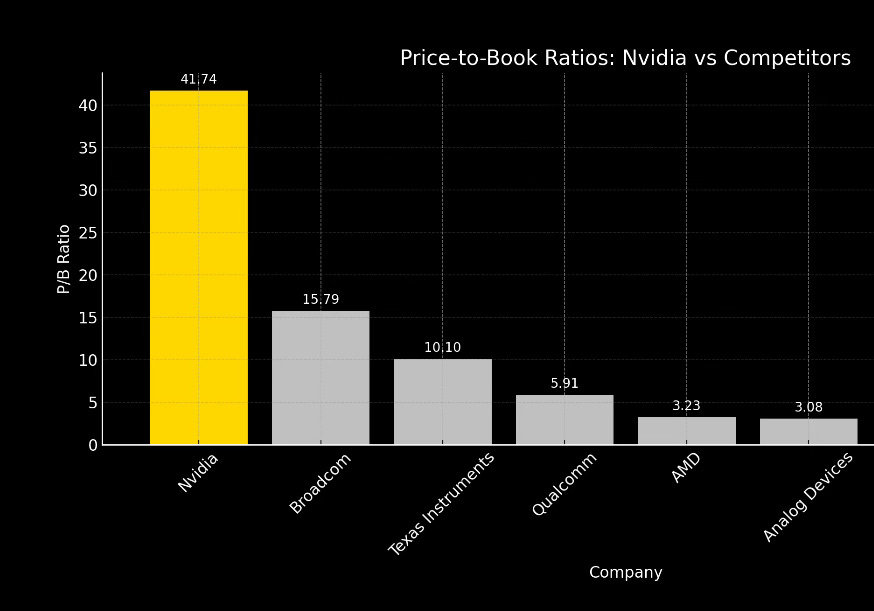

Valuation: The Deadly Sin of Greed

Before we even open the box, we find our first deadly sin: Greed. Nvidia’s valuation sits at heights so dizzying they could qualify as one of John Doe’s twisted moral lessons.

Price-to-Earnings (P/E): 50 — a shrine to market euphoria.

P/E at 50 means investors are paying for half a century of earnings today.

Price-to-Sales (P/S): 26 — unmatched by any semiconductor peer.

P/S at 26 says the market values every dollar of Nvidia’s sales as if it were a bar of gold.

Price-to-Book (P/B): 41 — financial gravity is clearly broken.

P/B at 41 suggests Nvidia is more myth than machinery. In the thematic framework of Se7en, these are not just numbers. They are confessions. We are watching a market indulgence in Gluttony, consuming valuation multiple after multiple until bloated beyond recognition.

Scene One: Opening the Box

Cue the desert. Cue the shadows. And cue the financial media headlines.

CNBC and others quickly latched onto a number: $0.96 earnings per share and a “BEAT”. That’s what Nvidia would have earned, they argue—if not for the $5.5 billion write-down tied to China export restrictions on its H20 chips. But that’s not the number that hit investors’ portfolios. That’s not the number in the box.

The real, adjusted EPS? $0.81.

And that’s where the confusion begins. Because some on Wall Street had slashed their forecasts to $0.75 after the China news broke. Others held to the original consensus of $0.88, or even higher (making it an earnings MISS). The result was a chaotic earnings moment: some media outlets called it a miss, others framed it as a beat.

Like the climax of Se7en, when the box hits the desert sand and Mills demands to know what’s inside, investors were left reeling—not from what was reported, but how it was spun. Nvidia didn’t lie. They simply nudged the spotlight. “Look over here,” they seemed to say, at that $0.96 ex-charge figure.

But the market, like Somerset, knows better. “We’re not just gonna walk in and take this.” Because what’s inside Nvidia’s earnings isn’t just a number—it’s a narrative. One shaped by interpretation, expectations, and a company that understands the power of framing.

Scene Two: The Crime Scene in the Financials

As the detective reads deeper into the filing, the room grows colder. Accounts receivable had ballooned in Q4 FY2025 to $23.1 billion, sending DSO to 53 days. That's Sloth—a laziness in collection masked as aggressive revenue recognition. It implies Nvidia was recognizing sales it hadn’t been paid for. Channel stuffing? Extended terms? The possibility lingers like a scent in the air.

Keep reading with a 7-day free trial

Subscribe to The Coastal Journal to keep reading this post and get 7 days of free access to the full post archives.