Nvidia Hits $4 Trillion in Market Cap

With this new world record, the question now is "Where are we going?"

With a $4 trillion market cap ( the world’s most valuable company) at $163 per share. But beneath the fanfare lies a deeper uncertainty—about valuation, sustainability, and direction.

Where are you going?

— Dave Matthews Band

That’s the question Dave Matthews poses in one of his most introspective songs. And it’s the same question Nvidia investors should now be asking.

The sheer scale of Nvidia’s rise is stunning. Its chips power AI data centers. Wall Street calls it the “back bone” of the artificial intelligence revolution. And yet, that very narrative is what makes the company so vulnerable going forward.

Because history has seen this movie before.

In the year 2000, Cisco Systems was the darling of the dot-com era. Its wireless routers and switches were the backbone of the Internet—a mission-critical infrastructure play that, just like Nvidia today, “you couldn’t build the internet without.” Cisco briefly became the most valuable company in the world, surpassing $550 billion in market cap and Microsoft. Its price-to-earnings ratio soared above 50x, and its price-to-sales ratio eclipsed 30x. These metrics weren’t just high—they were historically extreme.

And that’s where the parallels get dangerous.

Today, Nvidia trades at approximately 52x earnings, 30x sales, and nearly 47x book value.

To justify these valuations, Nvidia would need to grow its earnings by double digits for the next decade straight—without any macro shocks, competitive disruptions, or regulatory hurdles. In reality, maintaining this valuation would require Nvidia to add the equivalent of a Fortune 100 company’s profit every year. That’s not growth. That’s fantasy.

What’s even more alarming is how fast the stock moves in dollar terms. Nvidia often swings more than $5 per share in a single trading session. At a $4 trillion market cap, that equates to a daily swing of over $150 billion—more than its total annual revenue. Imagine that: the stock is now so large that it fluctuates in market cap each day by more than what the business produces in revenue per year.

You are grown weary?

— Dave Matthews Band

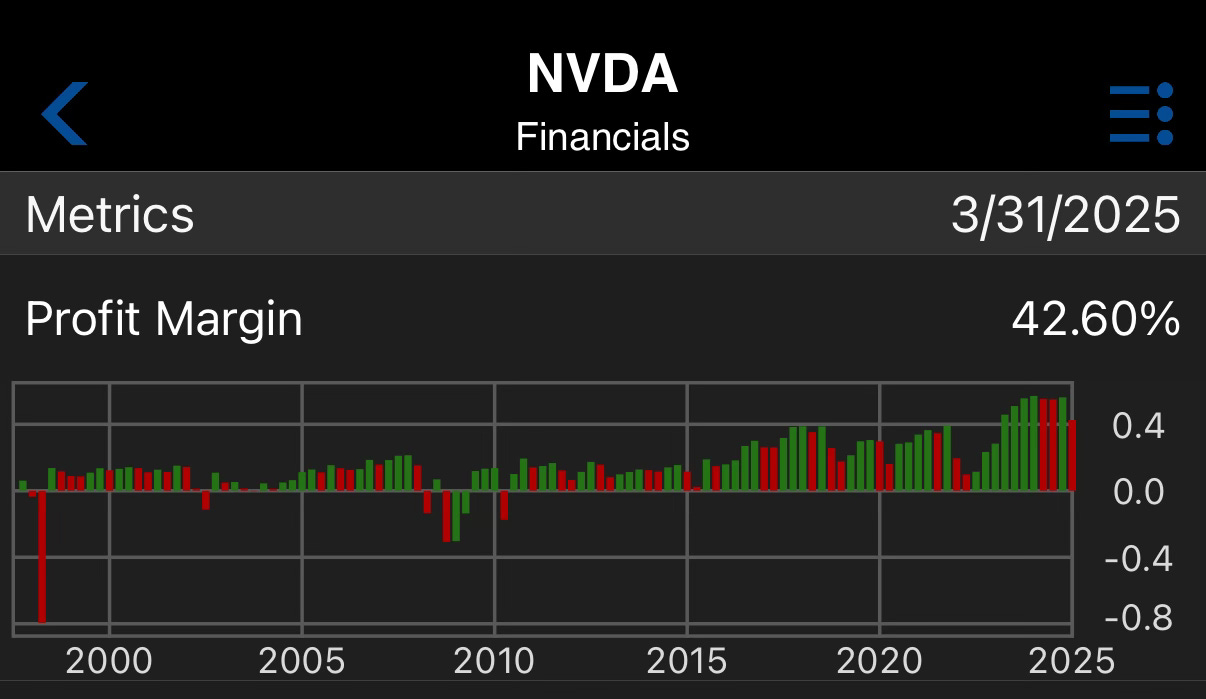

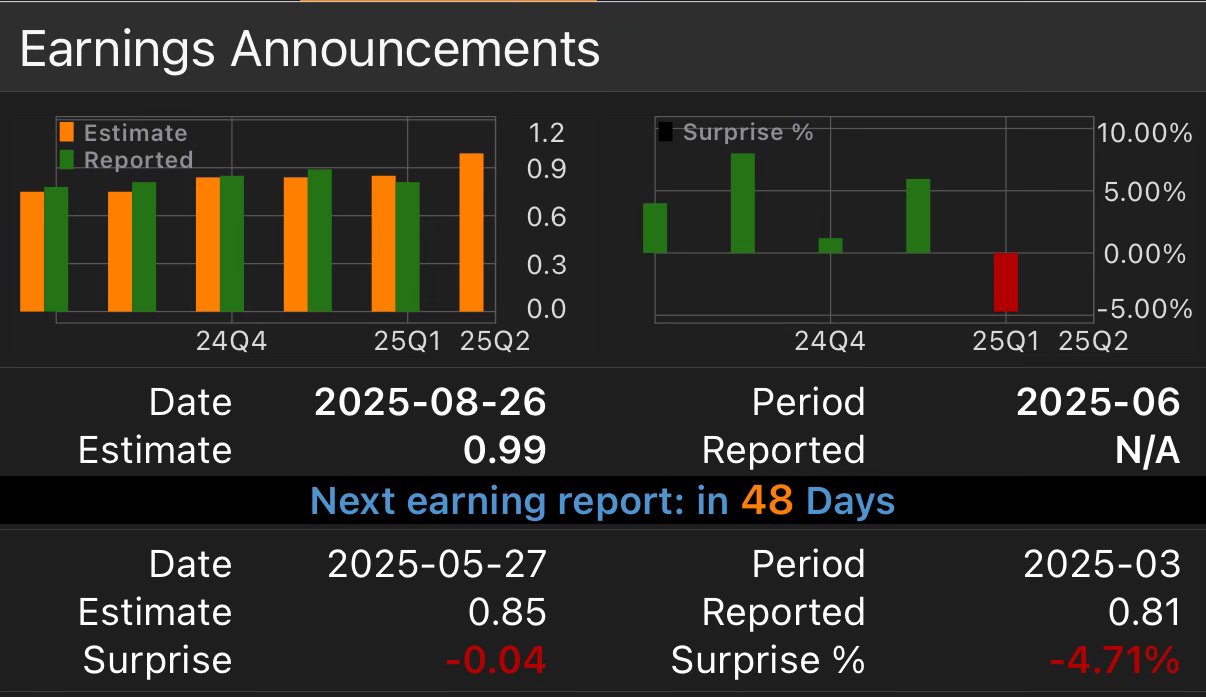

That lyric hits harder when you look at the company’s most recent earnings. Nvidia’s profit margins fell from 56% in Q4 2024 to just 43% in Q1 2025.

That’s not a rounding error—it’s a structural decline. Sequential earnings dropped -5%, largely due to Chinese export limitations and a slowdown in data center spending. ( so Nvidia excluded that metric to ‘beat” Wall Street earning estimates). But earnings in fact declined.

And yet, the market shrugged it off. The stock rallied on narrative, not on fundamentals.

Meanwhile, the company is pouring capital into financial engineering rather than foundational growth. In Q1 alone, Nvidia spent over $15 billion on buybacks and just $1.2 billion on capital expenditures. It is prioritizing short-term optics over long-term durability—a hallmark of late-cycle excess.

And that’s the problem. At this valuation, Nvidia must be Superman. It must meet every growth expectation, beat every earnings target, and hold off every competitor—every quarter. One misstep, and the $4 trillion illusion begins to fracture.

Under the Financial Hood: Nvidia’s Cash Flow Is Flashing Warnings

At $4 trillion in market cap, you’d expect Nvidia to be reinvesting aggressively—building new fabs, buying critical IP, or expanding into adjacent technologies. But a closer look at the company’s Q1 2025 cash flow statement tells a very different story. Behind the AI buzzwords and Wall Street cheerleading lies a capital deployment strategy that prioritizes appearances over durability.

Nvidia’s accounts receivable grew faster than cash flow in the past year—especially in Q4 FY2025, where AR spiked $5B while cash flow declined. Days Sales Outstanding (DSO) jumped from 41 to 53 days, suggesting customers are taking longer to pay—classic signs of looser terms or end-of-quarter sales pressure.

This pattern—ballooning AR + lagging cash flow—is a yellow flag for aggressive revenue recognition. No hard proof of channel stuffing yet, but if AR continues to outpace collections, it could point to deeper revenue quality issues.

[🔒 PAYWALL BEGINS HERE — Coastal Journal Full Access Team]

Keep reading with a 7-day free trial

Subscribe to The Coastal Journal to keep reading this post and get 7 days of free access to the full post archives.