Tesla Earnings Miss

Is this a Bull or a Bear Trap for Investors?

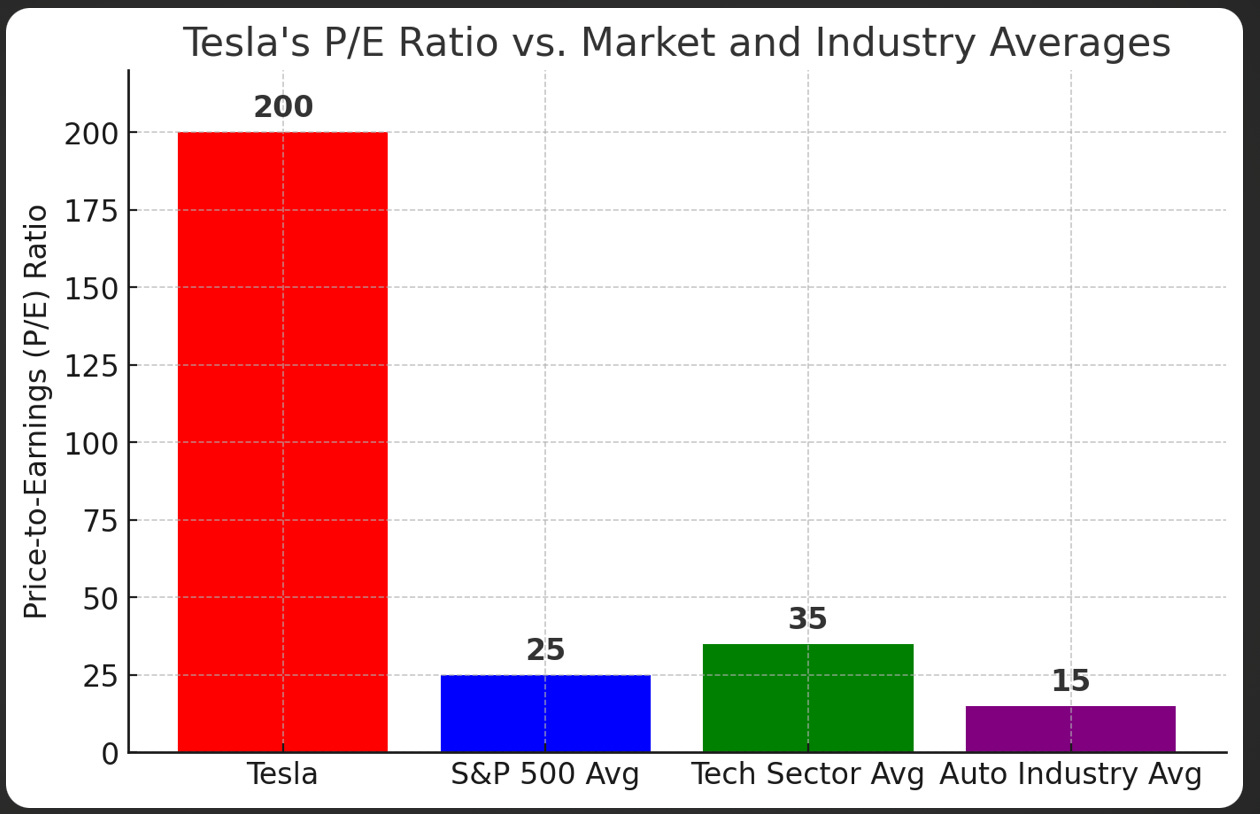

Tesla’s fourth-quarter earnings weren’t just a miss—they were a glaring warning sign for investors still clinging to the myth of limitless growth. With shares down nearly 20% from their $488 peak, now trading around $400, the EV giant reported an 8% drop in automotive revenue, falling short of Wall Street expectations and raising serious concerns about its lofty valuation. Slowing demand, shrinking margins, and the conspicuous absence of 2025 guidance paint a troubling picture. Yet, despite dismal earnings, Tesla’s stock remains elevated—sending its price-to-earnings (P/E) ratio soaring to 200x, a level that increasingly resembles a bubble on the brink of collapse.

Tesla’s Revenue Collapse Signals Cracks in the Foundation

For a company supposedly revolutionizing the auto industry, a year-over-year revenue decline is nothing short of catastrophic. Tesla’s automotive sales dropped 8%, from $21.56 billion to $19.8 billion, despite aggressive price cutson its Model 3, Model Y, and luxury Model S/X lineup. Instead of spurring demand, the markdowns only eroded profits—an ominous sign that Tesla’s once-insatiable consumer base may no longer be willing to pay the premium.

But perhaps the most chilling takeaway? Tesla refused to provide 2025 sales guidance—a glaring omission that all but confirms the company itself has no clear sense of demand trends. As the EV market grows more saturated with competitors, Tesla’s pricing power is crumbling, and its dominant position is facing an existential threat.

Tesla’s Valuation Defies Gravity—But for How Long?

The disparity between Tesla’s stock price and its actual business performance is staggering. Investors continue to price Tesla as if it were a high-growth tech juggernaut, when in reality, it’s behaving more and more like a mature automaker facing brutal competition.

Consider the numbers:

• P/E Ratio: 200 based on today’s earnings, compared to Ford (5.76) and General Motors (5.34).

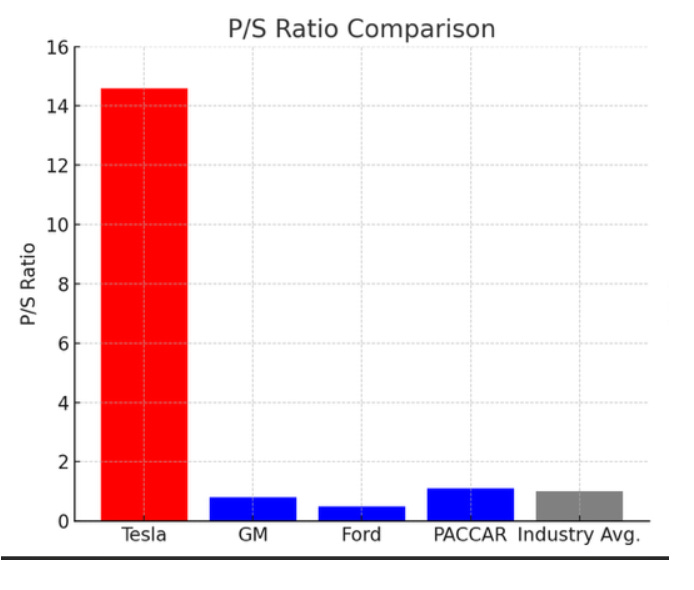

• P/S Ratio: 14.59, while most legacy automakers trade below 1.0.

• P/B Ratio: 18.65, in contrast to the auto industry average of under 5.0.

These absurdly inflated metrics imply that Tesla is in a league of its own—a company on an unrelenting growth trajectory with limitless expansion ahead. The problem? The numbers don’t back it up.

Tesla’s Bubble Is Fraying at the Edges

Tesla’s stock is priced for perfection, but its latest earnings reveal anything but. The combination of declining revenue, vanishing margins, and opaque guidance should be a major wake-up call for investors still clinging to the dream of endless growth. With competition rising and the market’s patience wearing thin, the cracks in Tesla’s valuation are becoming impossible to ignore.

The question now isn’t whether Tesla’s stock will correct—it’s how painful that correction will be.

A closer examination of Tesla’s financials paints a troubling picture—one that goes beyond slowing demand and shrinking margins. Beneath the surface, accounting maneuvers and financial engineering are propping up the numbers, masking the severity of Tesla’s operational struggles.

Tesla’s Profit Collapse: The Harsh Reality

Tesla’s earnings reveal a company in financial freefall:

• Net income (GAAP) imploded, plunging 70% from $7.9 billion in Q4 2023 to $2.3 billion in Q4 2024.

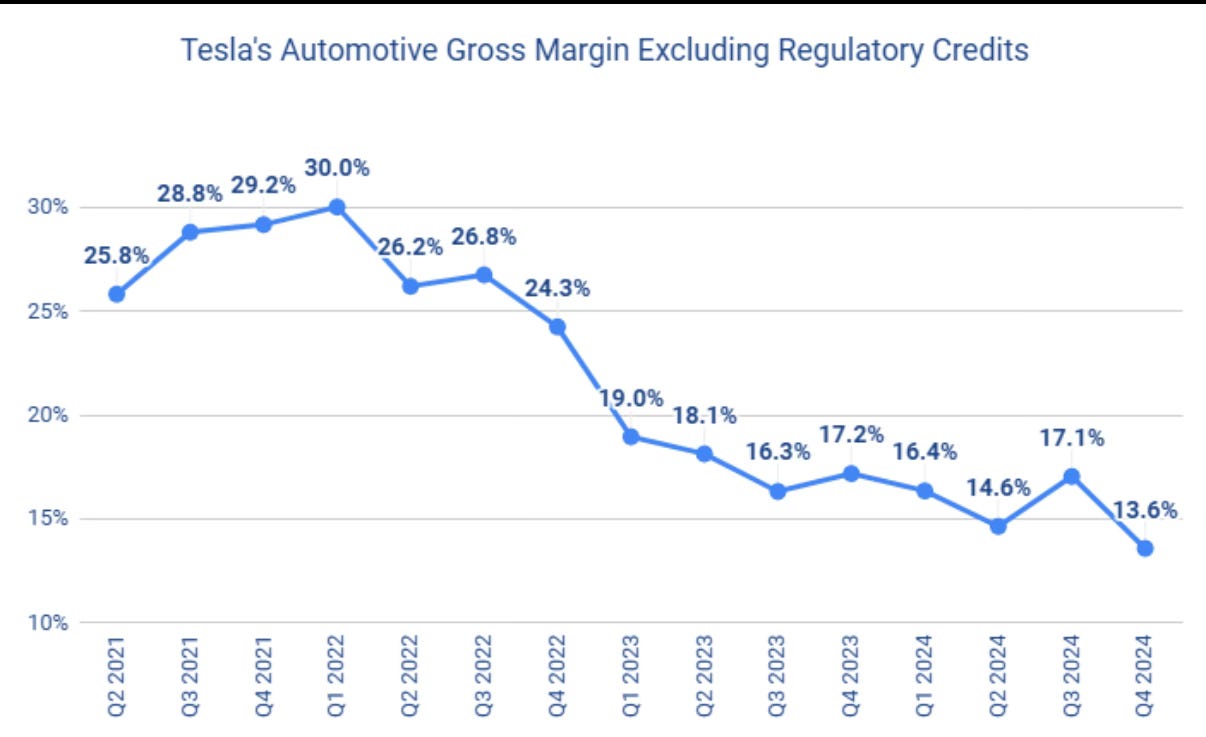

• Tesla’s Auto Gross margin nosedived, a direct consequence of relentless price cuts.

• EPS (GAAP) cratered from $2.27 to $0.66, exposing Tesla’s vanishing profitability.

Tesla’s strategy of slashing prices to sustain sales volume is proving to be a double-edged sword—one that erodes profits while failing to generate enough demand to offset the damage. CEO Elon Musk insists it’s a long-term play, but the short-term financial wreckage is undeniable.

Accounting Red Flags: How Tesla Manipulates the Numbers

Tesla’s latest filing reveals several questionable accounting tactics—moves that make earnings appear stronger than they actually are.

Keep reading with a 7-day free trial

Subscribe to The Coastal Journal to keep reading this post and get 7 days of free access to the full post archives.