Tesla Earnings Preview

The Most Overvalued AI Stock

Tesla’s upcoming earnings report looms like a storm on Wall Street’s horizon, and the stakes couldn’t be higher. With its forward price-to-earnings (P/E) ratio now soaring to an astronomical 135x, Tesla stands as both a symbol of boundless innovation and a case study in speculative risk. For a company facing declining car sales, bloated inventories, and reliance on precarious revenue streams, the illusion of invincibility could crumble this week—and with it, a significant piece of the current AI-driven market euphoria.

Wall Street’s Darling or a House of Cards?

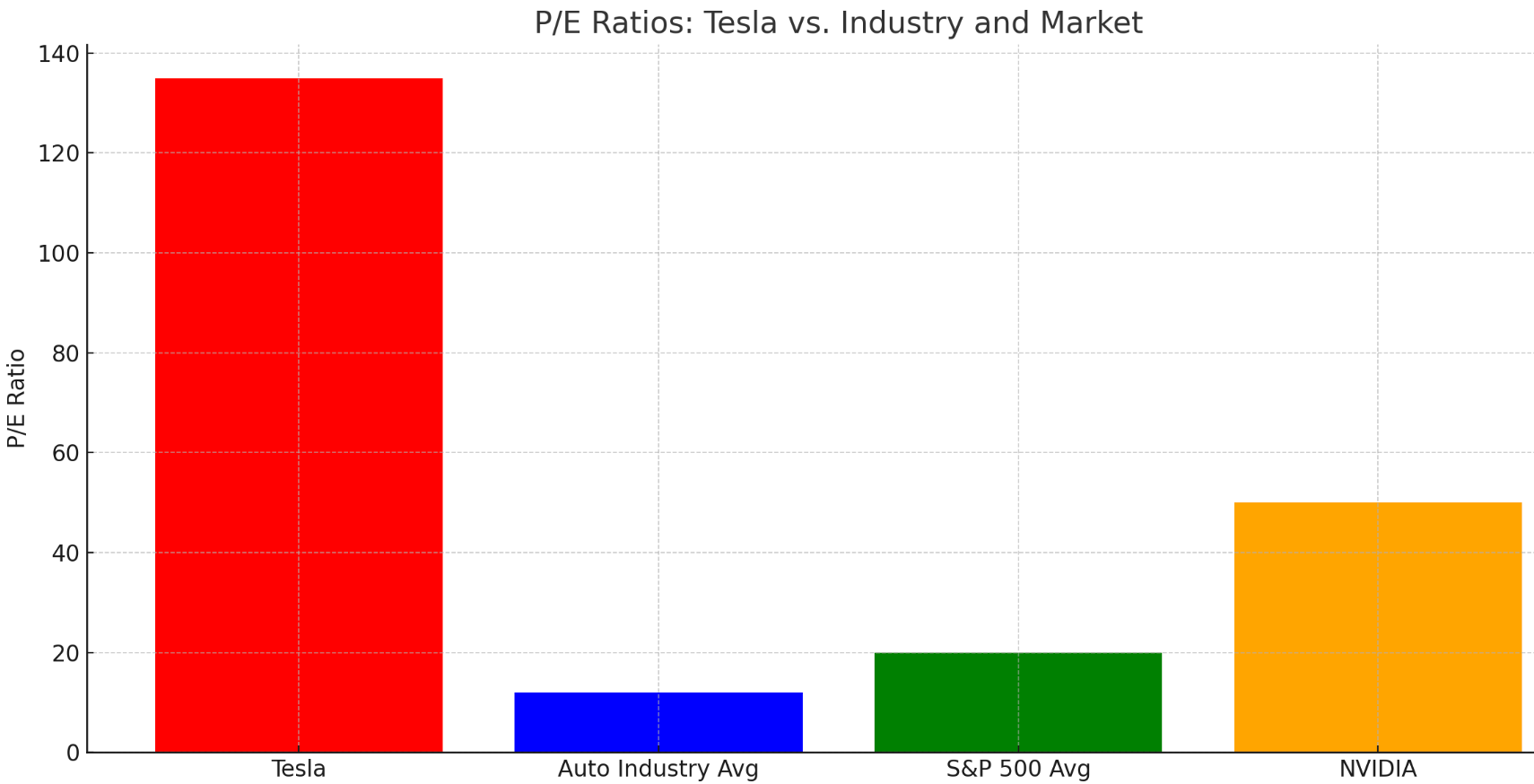

Tesla isn’t just another high-growth stock; it’s a juggernaut whose valuation defies traditional metrics. While the auto industry averages a modest 12x P/E ratio and even market darling NVIDIA clocks in at 50x, Tesla’s 135x figure feels closer to fantasy than finance. The numbers suggest perfection is priced in, but history is clear: when stocks are valued for infallibility, even the smallest cracks in the façade can lead to catastrophic sell-offs.

And the cracks are becoming harder to ignore.

The Evidence Piling Up Against Tesla

1. The P/E Illusion: A Dangerous Gamble on the Future

Tesla’s current valuation implies a fairy tale of limitless growth in revenue, profits, and market share. With 2025 earnings projected at just $3.50 per share, Tesla’s forward P/E ratio would still tower at 135x, a figure that assumes flawless execution and endless demand. Compare that to the broader S&P 500 average of 20x—or even tech titans like Apple and Microsoft, which hover in the 30x–40x range. One slip—a missed delivery target, a hiccup in production, or faltering demand—could send shares into a freefall.

2. Regulatory Credit Windfall: Temporary Salvation

Keep reading with a 7-day free trial

Subscribe to The Coastal Journal to keep reading this post and get 7 days of free access to the full post archives.