There Is Overvaluation in Stocks

“And it’s been the ruin of many a poor boy…”

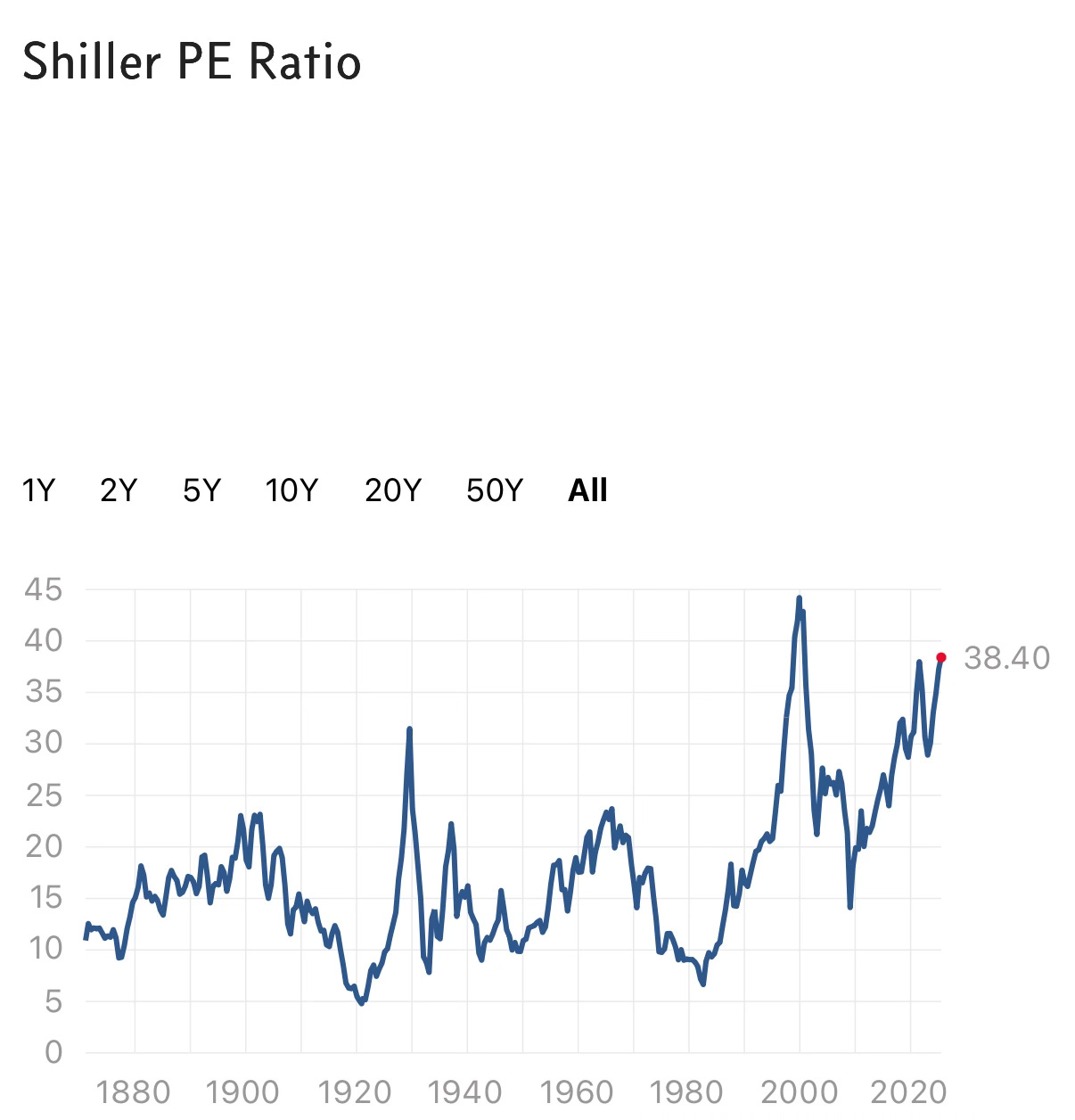

Consider this: the Shiller P/E ratio—also known as the cyclically adjusted price-to-earnings (CAPE) ratio—is now sitting at 38.4. That’s the second highest level in history, surpassed only once: during the peak of the dot-com bubble in 2000, when it briefly touched 44.

This isn’t just another valuation metric. Unlike the standard P/E ratio, which compares price to current earnings, the Shiller P/E smooths out earnings over the past 10 years—adjusted for inflation. It’s a long-term gauge designed to strip out the noise of temporary booms or busts and tell you when you’re paying too much for a dollar of earnings.

In 1929, before the Great Depression, the Shiller P/E hit ~30. In 2000, before the tech wreck, it hit 44. Today, at nearly 39, we’re on that same trajectory—and yet investors are treating these levels like business as usual.

That’s the backdrop for this earnings season. And it’s why the market feels like a House of the Rising Sun.

“There is a house in New Orleans / They call the Rising Sun / And it’s been the ruin of many a poor boy / And God, I know I’m one.”

There’s a house in this market they call the Rising Sun. It’s built not on fundamentals, but on speculation —speculation that AI will keep stock prices soaring that liquidity will remain endless, that prices always go up. And like the gamblers and drifters in the song, many investors have stumbled through its doors believing they were walking into fortune.

This week, they began learning the truth: that house doesn’t bless you—it breaks you.

Netflix: A Dream Priced for Perfection

Netflix was the first tech juggernaut to report. It beat expectations. But in this market, the beat isn’t the story. The valuation is.

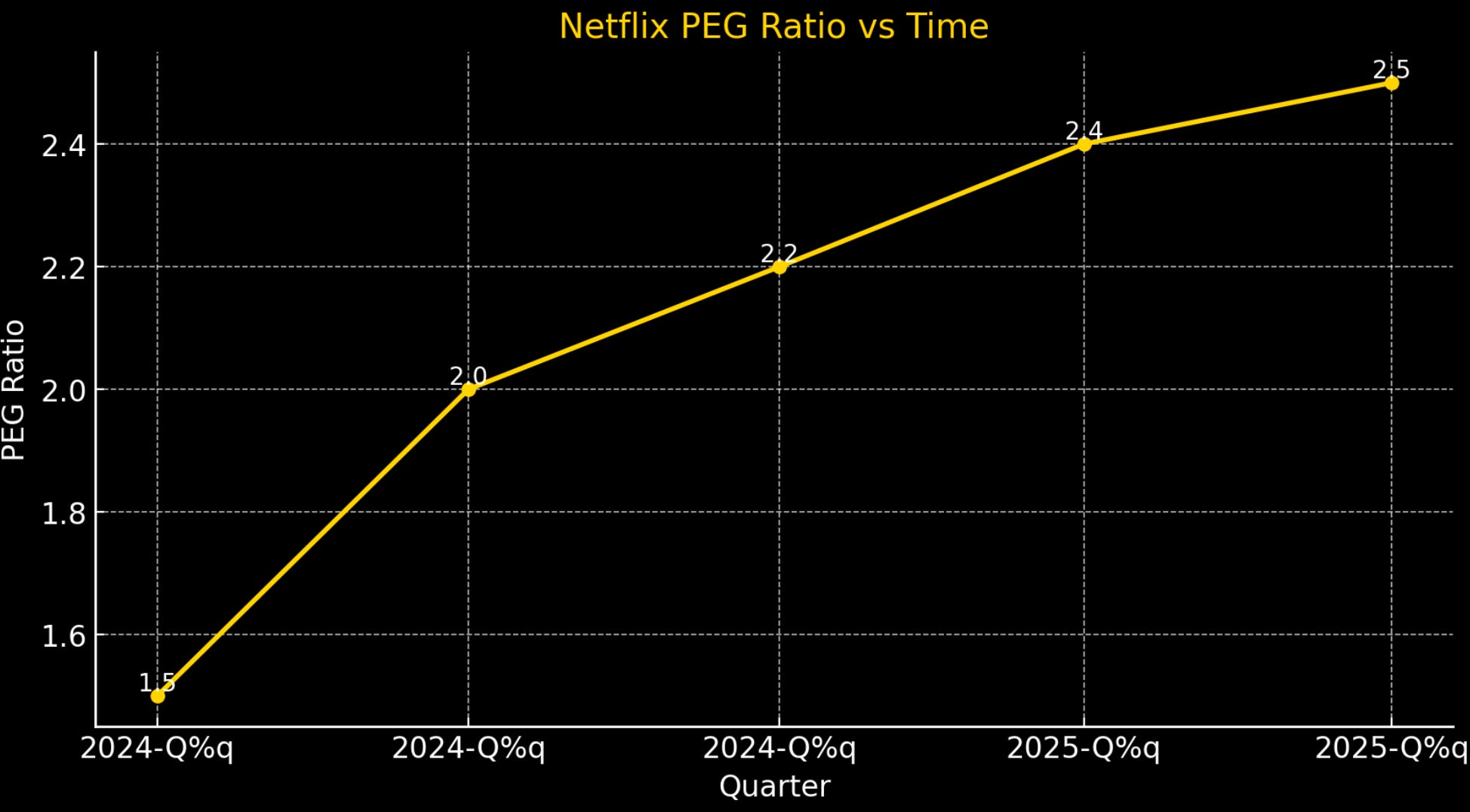

At $1,215 per share and $21 in annual earnings, Netflix now trades at 53 times earnings. That’s not just high. That’s a number that demands perpetual double-digit growth—growth that even Netflix isn’t forecasting.

To justify its current price without it crashing, the company would need to double its EPS to $42. At that point, the P/E would fall to a more reasonable 30. But there’s no indication Netflix can deliver that kind of earnings explosion—especially with projected growth stuck in the low double digits. The PEG ratio—a blend of price and expected growth—stands at 2.5, well above the danger zone. For context, anything over 2 is considered expensive. Netflix has blown past that, and Wall Street’s still calling it cheap.

“Now the only thing a gambler needs / Is a suitcase and trunk…”

Investing at this valuation isn’t investing. It’s gambling. And the longer the rally runs on fumes, the more brutal the hangover will be.

Smaller Banks Warning Signs

Western Alliance: Borrowing Its Way Through the Fire

On the surface, Western Alliance’s earnings looked stable. But when you read the filings—really read them—you find a bank borrowing at emergency levels just to stay operational.

🔒 [Full Coastal Journal Access below]

The headlines say “beats.” The filings say borrowed time.

$6.1B surge in Western Alliance debt

Ally at 65× P/E with shrinking deposits

HBAN capital + credit risk rising

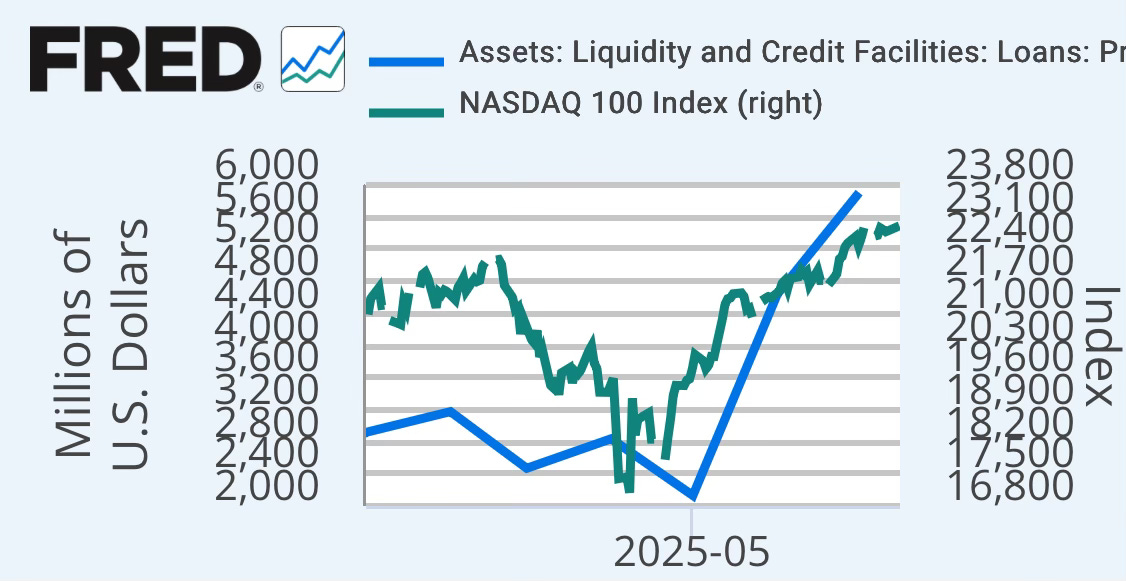

Fed Liquidity (Primary Credit / Discount Window) stays high

Get the red flags, the options play, and the real data below

👉 $10/month or $100/year

Keep reading with a 7-day free trial

Subscribe to The Coastal Journal to keep reading this post and get 7 days of free access to the full post archives.